Drug prices shift as COVID-19 begins making its mark on the supply chain

For the past 20 months, in the pre-COVID-19 era, we’ve released a monthly report called “What’s Happening To Generic Drug Prices,” where we track month-by-month price changes from the CMS National Average Drug Acquisition Cost (NADAC) survey of community pharmacy invoice acquisition costs for prescription drugs.

We’ve been pretty proud of this streak, but as they say, all streaks are meant to be broken. So we are going to re-purpose this month’s generic update to flood you with yet more COVID-19-related reading material. Not to worry though, for the very few die-hard WHTGDP readers out there, we’ll still provide the standard charts and figures later on in this update.

We were very much looking forward to the week of April 20th, 2020. This was the release week for the latest NADAC survey results – the first time that we were going to be able to see all of the moving parts that had been spun into motion due to COVID-19. You may have seen the dashboard that we created in anticipation of this day, our Abnormal Drug Price Increase Tracker (ADPIT) – which is designed to separate the drug pricing wheat from the chaff to pinpoint drugs that experienced abnormally large pricing movements. All we needed was to feed the tool pricing data smack in the middle of the COVID-19 surge, i.e. March’s pricing data. And that data was set to come this week.

There’s only one problem – we were wrong.

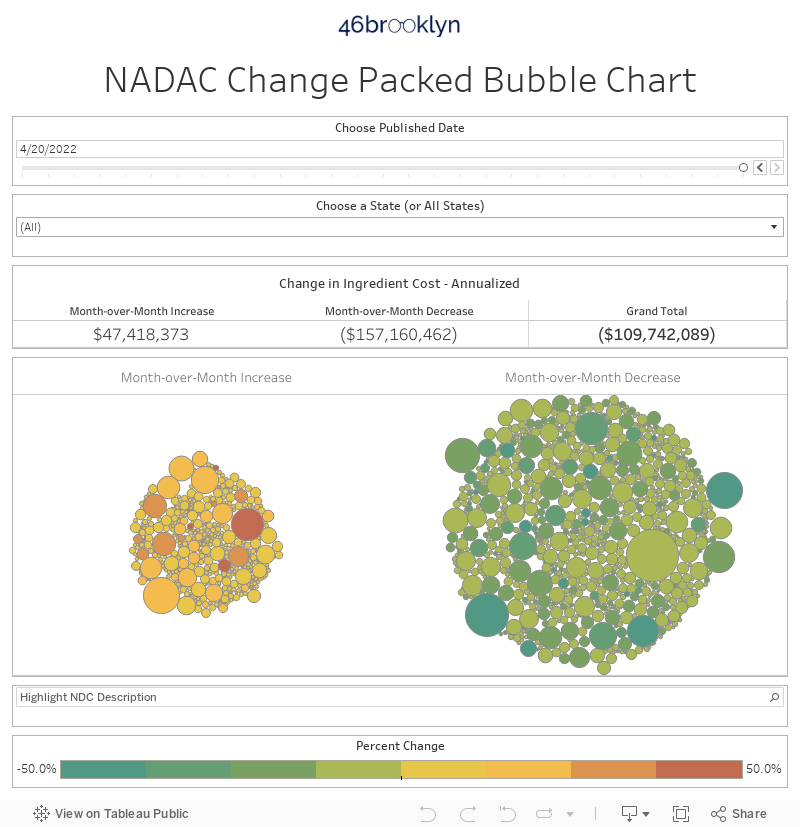

After racing to update our dashboards, we immediately suspected something was up when our NADAC Change Packed Bubble Chart showed a whopping $175 million in deflation based on Medicaid’s annualized drug mix. This is literally the largest monthly weighted deflation number we have seen since the generic deflation “glory days” (i.e. before 2019). Not only did it come in the middle of what very apparently is becoming a secular easing of generic deflation, but it also came in the exact month we expected to start seeing at least some erratic pricing movements either directly or indirectly due to COVID-19.

So with the principle of Occam’s Razor top of mind, we looked for the simplest answer to explain this perplexing result. This led us back to the NADAC Methodology document, which we admittedly have not perused in awhile. And there, illustrated very clearly on page 26 is the answer – “NADACs are posted two months after the surveyed pharmacy invoices are collected.”

Figure 1

Source: Medicaid.gov

So, it follows that the prices published this week reflect surveyed invoice prices from February 2020, firmly in the pre-COVID-19 era. On a positive note, we are grateful that this process forced us to research and slightly tweak one of our core assumptions about NADAC (which we will do across the handful of dashboards where we lag-effect NADAC – for you hardcore 46brooklyn-ers out there, this will cause many of the markups previously in Medicaid programs to slightly grow even larger). On a negative note, we now have to wait another month to:

See what happened to generic drug acquisition costs in March (which will be released on May 20th, to be precise), and

Really put ADPIT through a stress test to see if it can assist us in identifying drugs experiencing price spikes (in some, due to COVID-19) that are not getting media attention

That said, we are already seeing a few glimpses of ADPIT’s capabilities. So, before we return to this month’s NADAC generic deflation story (which was pretty epic and deserves some attention) let’s start off our key takeaway list with a few nuggets from Abnormal Drug Price Increase Tracker (ADPIT).

1. Naproxen (delayed release) prices continue to skyrocket

Last month, we reported on the 10x jump ($0.21 to $2.07) in naproxen delayed release tablets (that’s for the 500 mg tablets … although the 375 mg still accelerated a not too shabby 4.5x last month). Fast-forward one month, and this same drug stole the show once again, stepping up another 70% to $3.51 per tablet. Head over to ADPIT, select “Generic” from the Drug Type filter, and sort on the “Relative Impact Ratio” field (which measures how far this week’s price update is above the trailing 52-week 90th percentile price for each drug) from high-to-low, and you’ll find naproxen heading up the list. Note: “EC-Naproxen” is the authorized generic for EC-Naprosyn (brand-name naproxen).

Figure 2

Source: Data.Medicaid.gov, 46brooklyn Research

One thing you may notice from the above chart is that if you total up all naproxen Medicaid prescriptions over a year, it adds up to only 100,852 prescriptions. That’s 0.0001% of the total prescriptions dispensed in Medicaid over the same period. So clearly this means we shouldn’t care about this, right? Wrong.

Remember, our goal here is to explore and better understand the inner workings of the U.S. drug supply chain. And oftentimes the best case studies come from the “tail” of the generic marketplace – the off-the-beaten path, lower utilization generics that few are paying attention to. We can learn a lot from these smaller, more manageable case studies and then work to apply this knowledge to create a more robust and resilient supply chain.

So, let’s see what naproxen can teach us. We’ll focus on the 500 mg strength to not have to tell the story twice.

According to Elsevier’s Gold Standard Drug Database, today there are four different “manufacturers” of delayed release naproxen (excluding re-packagers, which trust us, you don’t want us to go down that rabbit hold right now): Cipla, Teva, Virtus, and Woodward.

Venture over to drugs@FDA, and look up delayed release naproxen and you’ll see that there are really only three approved applications:

NDA 020067 from applicant “ATNAHS PHARMA US”

ANDA 091432 from applicant “SUNRISE PHARM INC”

ANDA 075227 from “TEVA”

Clearly, some “manufacturers” (technically, they are called “labelers”) are distributing this drug off the same FDA application. We spent more time researching and found out that:

Woodward is marketing an authorized generic off NDA 020067

Teva is marketing a generic off ANDA 075227

Cipla, and Virtus are both marketing generics off ANDA 91432

This last group very much reminds us of the poster child of masked competition: generic Prilosec OTC (omeprazole OTC tablets), which have a half a dozen labelers all marketing off the same application, and seemingly sourcing their product from the same location.

This is why we believe that to get a true sense of the competitive landscape for a drug, we have to look at market share by application, in addition to market share by labeler, which is exactly what we do in our Medicaid Drug Market Share Dashboard. This was our next stop on our naproxen journey.

Figure 3 shows Medicaid market share for Q3 2019, the latest quarter of available Medicaid data. The top chart is market share by FDA applicant, while the bottom is market share by labeler. In this case, they line up fairly well – Cipla has dominant market share at 82.5%, followed by Teva at 11.1%, and Woodward at 6.3%. Three labelers that have gained some sort of traction in Medicaid (Virtus didn’t come to market until Nov 2019), which clearly is highly skewed to just one – Cipla.

Figure 3

Source: Data.Medicaid.gov, Elsevier Gold Standard Drug Database, Drugs@FDA, 46brooklyn Research

Now to be clear, back in Q3 2019, this drug was still just ~$0.20 per tablet, and had been rock solid at this level for years. But such heavy market concentration is a fairly tenuous position to be in for a drug. It’s exactly the position the now-famous hydroxychloroquine was in in early 2014 before the FDA slapped import restrictions on Ranbaxy (who at the time, had >80% Medicaid market share):

Figure 4

Source: Data.Medicaid.gov, Drugs@FDA, 46brooklyn Research

Lo and behold, wipe out 80% of the market for hydroxychloroquine, and look what happens to the price! As you can see in Figure 5, it goes from $0.10 per tablet to $2.26 per tablet – eerily similar to the magnitude of the price spike we are now seeing on delayed release naproxen.

Figure 5

Source: Data.Medicaid.gov, 46brooklyn Research

This would suggest that something has happened to Cipla, the dominant player in delayed release naproxen market. Did Cipla increase its prices? Or did it exit the market?

Hold onto those questions. Before we reveal what we suspect happened, we have to provide some context on how pharmacies purchase generic drugs, and to do that, we need to first talk about toilet paper.

Rewind back two months ago, and try to recall a trip to your grocery store. At some point during this trip, you probably arrived in front of an impressive white wall of toilet paper and spent a few seconds contemplating the dozen or so options you have for handling your delicate business. Were you feeling frugal and up for braving the grating feeling of the cheap store brand? Or did that exceedingly happy bear on the packaging convince you to splurge on the $10 Charmin Ultra Soft Mega Roll?

For sake of this extended analogy, let’s assume that everyone views toilet paper as a pure commodity. Toilet paper is toilet paper. You wipe with it. You flush it. Branding aside, why spend more than you have to? Assuming this is the case, you pick up the least expensive package and walk out. Toilet paper costs $5.

Our trip to the toilet paper aisle, Ben’s grocery store of choice - March 14th, 2020

Fast forward two months into the heart of COVID-19. You don your mask and venture back out to the same grocery store, but instead of coming across a glistening white wall of toilet paper, you are confronted with ransacked empty shelves. But luckily within the void, you catch that happy-go-lucky Charmin bear staring at you (who remains far too happy given the circumstances). Without any other options, you grab the Charmin Ultra Soft Mega Roll and bolt for the cashier, grateful that you won’t have to resort to other means. Toilet paper now costs $10.

So in this scenario, from two months ago to now, if we agree that toilet paper is a fungible commodity, the price of toilet paper went up. Note that no manufacturer increased its price here. Instead, what happened is what in corporate finance lingo is called “unfavorable mix shift” (favorable if you are the manufacturer though). You were forced to switch from a cheap option to an expensive option, driving the cost of the fungible product up.

This is very similar to how pharmacies buy generic drugs from their wholesalers. Each day they log in to make purchases, they are confronted with dozens of options to purchase for each fungible generic drug they need. Should I purchase the 1,000 count bottle of atorvastatin 10 mg made by Ascend? Or maybe the 500 count bottle of atorvastatin 10 mg made by Dr. Reddy’s? The answer is, with very few exceptions, pharmacies (that want to remain in business) simply purchase the cheapest one. If their wholesaler prices Dr. Reddy’s at a few pennies per pill cheaper than Ascend, then it will shoot to the top of the list, and likely end up on the pharmacy’s shelf the next day. In this way, generics are pure commodities. No fuzzy cute bears and marketing slogans. Just cost.

But what happens when the wholesaler no longer has Dr. Reddy’s? The pharmacy will simply buy the next cheapest option (let’s say Ascend), and the pharmacy’s cost will rise ever so slightly. What happens the if say, Ascend decided to discontinue production? The pharmacy moves to the next cheapest option, and so on.

For a heavily utilized drug like atorvastatin, there are plenty of manufacturers willing to produce at very low prices. So, even if the lowest cost ones drop out, all of this may go unnoticed. But that’s not the case with delayed release naproxen, which was largely dominated by two labelers (Cipla and Teva). Manufacturers/wholesalers were apparently (for at least a few years) very happy to sell this drug somewhere in the neighborhood of $0.20 per tablet, creating a tenuous stability of sorts. But what if they changed their mind and decided this wasn’t worth it anymore? Who else would sell it? And for how much?

Well, we now have our answer to our earlier question related to naproxen DR. We called several pharmacies and asked if they could buy Teva or Cipla from their primary wholesalers. They couldn’t. Beyond that, some received messages that the product was discontinued (to be clear, it’s not marked inactive yet, but pharmacies tend to see this far earlier than when it’s reported to drug information databases). The next cheapest option? Well, there are really only two – Virtus (the only remaining generic) and Woodward (an authorized generic). And those are going to run pharmacies more than $2 a tablet (at least), which explains why NADAC has rapidly spiked.

Please note, we are not passing judgment on this situation. It is neither good nor bad. It just is the way this works. If Cipla and Teva exited the market (which to be clear, we have not confirmed beyond our sleuthing), they may have done so because the economics for this drug simply didn’t work, and it was easier to rationalize exiting the market than raising prices in an era of intense price scrutiny. And maybe Virtus’ and Woodwards’ costs are materially higher than Cipla’s and Teva’s, justifying higher price at wholesalers? We don’t know.

The key takeaway here is that you don’t need to have “price increases” to have price increases. For generic drugs, “mix shifts” can do the job. And for the hundreds (maybe thousands?) of drugs that are on the lower end of the utilization spectrum that only have a few labelers, these mix shifts can be fast and extreme. One day a drug may be a cost-effective and efficient option for treating an indication. The next day it isn’t.

You’ve been warned! Perhaps now more than ever, payers should make sure that they or their PBM have processes in place to make timely formulary adjustments as generic prices change.

2. Tacrolimus prices jump, just months before being added to COVID trials

Another drug of interest that rose to the top of ADPIT was generic Prograf (tacrolimus), an immunosuppressive drug primarily used to prevent rejection after an organ transplant. As shown below, the 1 mg strength of the drug bottomed out at $0.19 per tablet in mid 2019. Now its up to $0.69 per tablet, following a 57% jump this month.

Figure 6

Source: Data.Medicaid.gov, 46brooklyn Research

As a reminder, this $0.69 per capsule cost reflects surveyed pharmacy invoice costs from February. Against this inflationary backdrop, a COVID-19 clinical trial including tacrolimus was just posted on ClinicalTrials.gov, making tacrolimus yet another case study of a drug prospect with already rising pre-COVID trial prices.

For the interested but unfamiliar, one of the first principles taught in infectious disease and immunology is that immunosuppresants like tacrolimus increase the risks for infections. So why then is tacrolimus being studied as part of treating an infectious disease like COVID-19? Apparently, it is related to clinical evidence suggesting that a sub-group of patients with severe COVID-19 develop a “cytokine storm.”

We do not blame you if that sounds like something out of a sci-fi movie, but simply put, the idea is that as the body works to fight off the infection (which it does by releasing chemicals called cytokines), it gets carried away and goes into overdrive (or storms off), causing more harm than good. Indeed, the researchers of the tacrolimus & COVID-19 study state, “Our working hypothesis is that severe COVID-19 pneumonia is secondary to a deleterious inflammatory process.” As with most things COVID-19-related, we will have to wait and see whether such treatment protocols are successful and whether the use of these drugs in these trial settings will add additional upward pricing pressure.

3. Latest COVID-19 clinical trial drug counts

On that note, we’ve been keeping track of all of the active ingredients that are currently undergoing trials in some way related to COVID-19. You can download our latest list here, which is updated through April 21. As a reminder, you can access this anytime on the ADPIT page. We’ll try to update it every Tuesday until it’s no longer relevant!

Here’s a quick snapshot showing the explosion in trials since we started keeping track just 14 days ago.

Figure 7

Source: ClinicalTrials.gov

For those who do not want to do the math, in the two weeks we’ve been monitoring the Clinical Trial data for COVID-19, the overall number of trials has grown by 82%, and the number of drug-related trials has grown by 70%! It only feels right to take a moment and thank the many scientists actively working to help us better combat this disease.

4. Mytesi’s price more than triples

For those of you that read Axios Vitals, Bob Herman’s scoop this morning was about the more than tripling of the brand-name drug Mytesi (crofelemer), a botanical drug for the treatment of diarrhea associated with the use of medications to treat HIV. As told by Herman, Jaguar Health increased Mytesi’s package price by 230% (from $668.52 to $2,206.52) after the FDA denied its request to authorize emergency use for treatment of COVID-19 patients. Jaguar argued that the price increase was necessary “to stave off the company’s collapse,” which after a quick glance at the “Sources of Liquidity” section in its latest SEC filings, very much appears to be a valid concern.

We should note that this price increase was technically reported into the public domain back on Tuesday. Where could you have found it? It’s in NADAC! Or a tool like ADPIT, which leverages NADAC prices.

There may be some confusion here, because we started off this report by lamenting the lag in NADAC survey reporting. But this is only true for generic drugs. Brand drugs (like Mytesi) are a completely different story. For brand drugs dispensed at retail pharmacies, “the NADACs … are reviewed and adjusted as necessary based on changes in published prices … on a weekly basis.” The NADAC Methodology document goes on to state that, “if the published price for a drug increases by 5%, then the NADAC for that drug is also increased by 5% … The relationship between changes in published brand drug prices and changes in actual brand drug prices obtained from surveys are tracked and monitored to ensure that a consistent correlation continues to exist.”

OK, Myers & Stauffer, it’s test time. For this statement to hold true, we should see a 230% increase in Mytesi’s NADAC this week, matching the 230% increase in its published price. To check, simply venture back over to the ADPIT tool, flip the switch to “Brand” name medications, and sort from high to low on Relative Impact Score, Despite its minuscule Medicaid volume, Mytesi marches right to the top of the list due to the magnitude of the increase. Hover over the trend chart at the bottom right, and you’ll see that Mytesi’s per unit NADAC went from $10.83 to $35.73, a 230% increase.

Figure 8

Source: Data.Medicaid.gov, 46brooklyn Research

It’s worth noting that you can find this information in a few other 46brooklyn visualizations.

Figure 9

Source: Data.Medicaid.gov, Elsevier Gold Standard Drug Database (GSDD), 46brooklyn Research

And our Brand Drug Price Change Box Score:

Figure 10

Source: Medicaid.gov, FDA.gov, 46brooklyn Research

5. Back to this month’s generic deflation … The number of drugs that decreased in price trounces those that increased in price

Each month, we first look at how many generic drugs went up and down in the latest month’s survey of retail pharmacy acquisition costs, and compare that to the prior month. As shown in Figure 11, April was an absolute deflationary beat-down. The number of generics with decreases vastly outnumbered those with increases – by a ratio of 1.7 to 1, the highest we have seen since we started tracking this in August 2018.

Basically, the quick way to read the chart below is to look for blue bars that are taller than orange bars to the left of the dotted line and exactly the opposite to the right of the dotted line. That would indicate a good month – more generic drugs going down in price compared to the prior month, and less drug prices going up. Again, this month was (very surprisingly) the best unweighted deflationary month we have seen since our inception.

Figure 11

Source: Data.Medicaid.gov, 46brooklyn Research

6. Weighted Medicaid generic deflation comes in at $175 million

As we’ve written in prior updates, knowing the price changes alone are not enough. We need to apply utilization (drug mix) to the price changes, which is the purpose of the NADAC Change Packed Bubble Chart (embedded again below). We use Medicaid’s Q4 2018 through Q3 2019 drug mix to arrive at an estimate of the total dollar impact of the latest NADAC pricing update. This helps quantify the real impact of those price changes from a payer’s perspective.

The green bubbles on the right of the above viz are the generic drugs that experienced a price decline in the latest survey, while the yellow/orange/red bubbles on the left are those drugs that experienced a price increase. The size of each bubble represents the dollar impact of the drug on Medicaid, based on utilization of the drug in the most recent trailing 12-month period. Stated differently, we simply multiply the latest survey price change by aggregate drug utilization in Medicaid over the past year, add up all the bubbles, and we get the total inflation/deflation impact of the survey changes.

Put it all together, and the weighted impact to Medicaid of the latest monthly survey was $175 million of generic deflation. A bonafide generic deflation blowout. That said, we should start seeing signs next month if COVID-19 related disruptions are going to put an end to this party.

7. Year-over-year generic oral solid deflation inches back up

But let’s put this in perspective. As shown in Figure 12, this blockbuster deflationary month ended up only slightly pushing up year-over-year deflation. Oral solid deflation crept up from 6.8% to 7.2%, while deflation on all generic drugs rose from 4.8% to 5.6%.

Figure 12

Source: Data.Medicaid.gov, 46brooklyn Research

In all, there are some fascinating takeaways this month. Be sure to peruse our dashboards, and let us know what you’re seeing.

Thanks to John Wilkerson at Inside Health Policy for his write-up on our new Abnormal Drug Price Increase Tracker.

Additional thanks to Charles Lyons, who profiled some of our work and insights on the Arnold Ventures site in a feature on COVID-19’s impact on the prescription drug supply chain.