Newly released CMS drug pricing data reveals continued generic drug pricing distortions

Let’s build some data!

Last Thursday, we devoted a day to filming our first video! As you can tell from the riveting title, “Tutorial of How to Construct the Medicaid Heat Map Database,” this sure-to-be critically-acclaimed short video will likely rival “This Is Us” in the intense, raw, emotions it will effortlessly evoke…

A picture of Eric getting ready to build the Medicaid Heat Map database in front of a camera. Much harder than anticipated!

All joking aside, we are really excited to be able to walk folks through exactly how to build the database that lives behind our first, and most popular, visualization. Hopefully, sharing our process will inspire more people out there to grab some data and use it to find answers to their drug pricing questions. If there is one thing we have learned over the past nine months, the prescription drug supply chain (and the data it wrongly thought was hidden) has produced a plethora of really ugly questions for us to explore. Way too many questions, way too little time. So we sure need all the help we can get.

We want to extend a heartfelt thank you to Ben Rivet at Journeyman Productions for dragging us through the process. We can’t wait to see (and share) the finished product.

Christmas comes early

As we began filming our video, we started by working through Step 1 of the process, which as you may expect is “Downloading the Data,” and noticed that CMS’ State Utilization Data was updated on May 8th. Recall that this dataset is a quarterly breakdown of what state Medicaid programs were essentially charged for prescription drugs (which . Given how delayed Q3 2018 data was, we were not expecting Q4 2018 data to be released in early May; yet here was a timestamp from last Wednesday.

It turns out that Christmas came early for us. Q4 2018 data is officially out … right in time for Mother’s Day weekend! Thanks a lot, CMS. 😩

Given our desire to maintain at least somewhat healthy marriages, we updated the visualizations that we could update quickly (Heat Map, Markup Universe, and Top 20 Over $20) and have prepared some highlights for you.

But we’re not done with this new data set. More is coming. There is just too much treasure in this data for those looking for hard facts to better hold this supply chain accountable. Hopefully, if our video is effective, there will be more treasure hunters out there – a lot more people passionate about seeking the truth on how drugs are really priced. We believe that by having more eyeballs on drug pricing data, we can ensure more details are scrutinized, because when it comes to drug prices, it really is all about the details.

With a new army of individuals analyzing drug pricing data and publishing their findings, we also look forward to the follow-up wave of projects for the team at Visante.

That said, here’s our first round of takeaways from the Q4 2018 state utilization data release.

Hello, Ohio pharmacies. Here’s a dollar. Good Luck.

Last month, we wrote all about Ohio’s data reporting change in Q3 2018, which for the first time allowed us to use public data to see what pharmacies were getting paid to dispense drugs in Medicaid managed care. Long story short, in July 2018, Ohio Medicaid required managed care organizations to switch from reporting what they paid to the PBM to what the PBM paid to the pharmacy. We then wrote an extraordinarily verbose report looking to identify drugs that seemed to be targeted by PBMs for “spread pricing” by comparing managed care cost in Q3 2018 to Q2 2018. It was such an long, meandering read, that we only expected a handful of folks to read it. Much to our surprise, the report has 14,874 page views (and counting). Go figure.

As we wrote, one of our concerns in sharing our analysis was that Ohio’s Q3 2018 data was incomplete. But after seeing the prices of so many generic drugs drop to just around pharmacy invoice acquisition costs (using NADAC), we trusted our gut that this was not a data issue that would clear up once the full Q3 2018 data was reported.

Boy, are we glad we did.

Recall that we presented charts for some of the most notorious high-markup generic drugs, showing all of them cratering in cost in Q3 2018, conveniently to a number right around NADAC. As a reminder, these drugs were:

generic Ziagen (abacavir)

generic Abilify (aripiprazole)

generic Nexium (esomeprazole magnesium)

generic Invega (paliperidone)

generic Crestor (rosuvastatin calcium)

generic Prograf (tacrolimus)

Take a look at these drugs now 👇. Not only does Q3 2018 managed care cost still line up with NADAC, but Q4 2018 managed care cost does as well! Any sliver of a chance that this was just coincidence is now gone.

For these drugs (and a lot more), it appears that criticisms of NADAC as a pricing benchmark may be a bit overblown, considering that NADAC appears to be right on the mark for where PBMs are setting their pharmacy prices. How cool is that? Ohio Medicaid essentially paid its managed care PBMs more than $6 per claim to yield the equivalent of something that could be downloaded for free.

Click the arrows to flip from one chart to the next

Of course, our critics will tell you it’s more complicated than this. And they are right – it is. So pay your PBM for all of those other complicated and costly functions such as utilization management (assuming they are actually doing that well for you). Just don’t pay much for generic drug rate-setting, because if the drugs above are any indication, you could do as good of a job with an Excel spreadsheet.

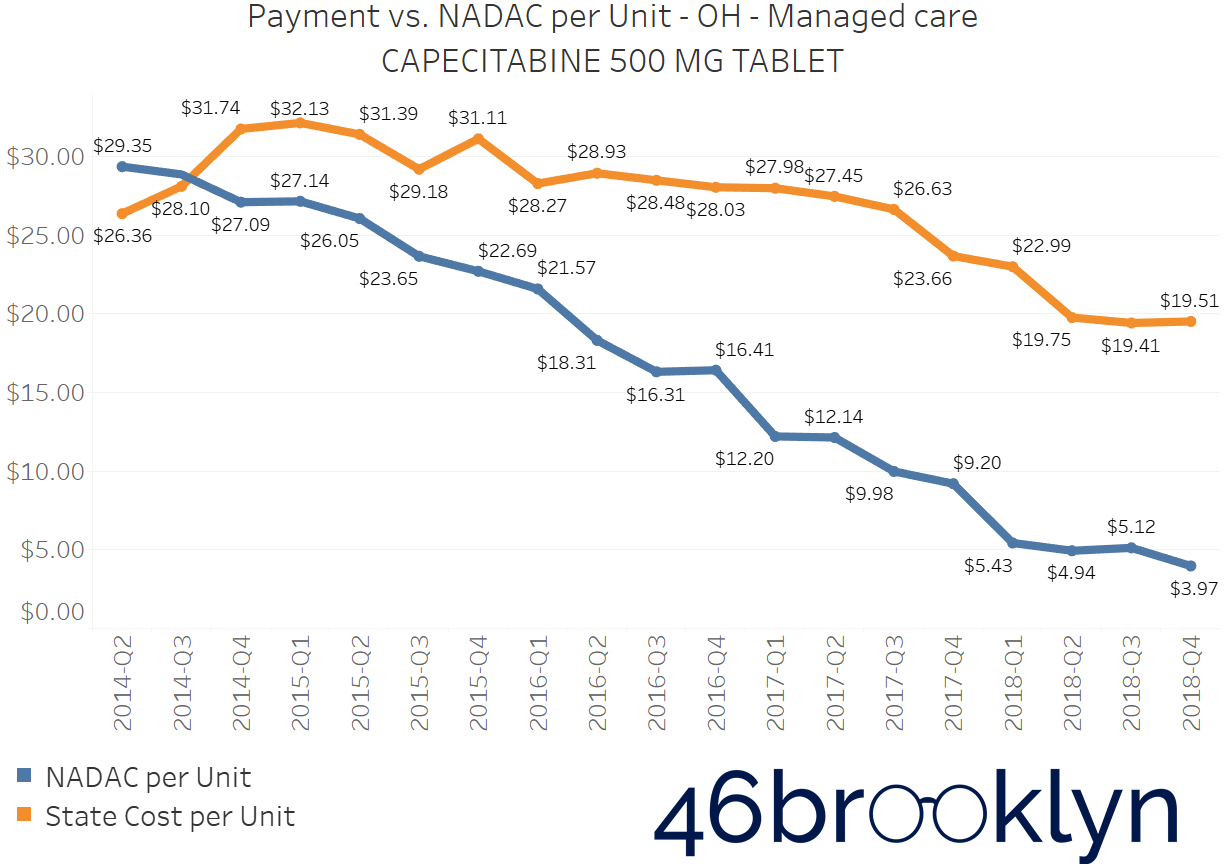

Figure 1 shows the weighted average managed care cost vs. NADAC for all generic oral solids in Ohio. The markup in Q4 2018 shrunk to a paltry 3 cents per unit. In Q4 2018, there were, on average, 40 units in each prescription. That means managed care PBMs paid Ohio pharmacies a margin over NADAC of $1.20 per generic oral solid prescription in Q4 2018.

Figure 1

Source: Data.Medicaid.gov, 46brooklyn Research

While we have been criticized for focusing on oral solids, we’ve been very clear that we only work with data we know we can trust. There is unfortunately no way to know what units of measure states are reporting for creams, ointments, powders, pens, vials, etc (i.e. non oral solids). This is because CMS doesn’t report the units of measure field in the State Utilization Database.

To illustrate the problem here, let’s look at Kristalose 20 gram Packets, which was highlighted by Visante in a lengthy retort to our work that we will address later in this report. As you’ll see in their analysis that criticizes 46brooklyn for focusing on oral solids, they highlight a number of “non-oral solids” that according to the pharmacy business specialists at Visante, appear to exhibit what they dub as “Negative Spread.” Let’s spend a minute investigating this claim.

First, we must figure out the units of measure for Kristalose 20 gram Packets. Is it packets? Or is it grams? We do know that NADAC’s unit cost for this drug is per packet. We of course don’t know what units are reported by states to CMS and then rolled up into the state utilization database. But for giggles what if we assumed that State Utilization Data for this drug was reported per gram? Then there would be twenty times the units (compared to NADAC), right? So what would happen if you multiplied a per-packet NADAC by per-gram state utilization data? You would get a Total NADAC that is roughly twenty times the Total MCO Reimbursed amount reported by the state. Just like Visante shows in Figure 2. Of course, there is simply no way to be sure this is what is happening, but we’ll just go ahead and trust Occam’s Razor on this one.

Figure 2

Source: Visante (annotated by 46brooklyn Research)

If you divide the Total NADAC presented by Visante for this drug by 20 (to convert from packets to grams), you will actually find out that this supposed “Negative Spread” drug is likely just another positive markup drug dressed up in unit-mismatch clothing. As you can see in Figure 2, there could be several “Negative Spread” drugs wearing this same costume. We just don’t know, and that’s why we avoid them in our analysis.

But we are grateful that PCMA and Visante have brought up this important topic, because this limitation is going to become increasingly problematic going forward. That’s because most new egregiously expensive specialty medications will fall into the non-oral solid bucket. Hopefully, CMS will work with states to apply and enforce reporting standards in both NADAC and State Utilization Data so we can all have better visibility into the pricing of the majority of specialty drugs going forward.

On another front, consider this … 74% of all prescriptions dispensed in Ohio Medicaid managed care were generic oral solids in Q4 2018. So looking at generic oral solids is quite relevant, especially for pharmacies that are getting paid around a buck over cost (before paying the pharmacist, technicians, rent, software expenses, transmission fees, etc.) on three quarters of the prescriptions they dispense to Medicaid managed care patients. This would seem to explain why pharmacies in Ohio continue to get the Daenerys Targaryen treatment.

Number of Prescriptions Dispensed in Ohio Managed care Medicaid in Q4 2018 (In Millions)*

Specialty Generics are still priced in the stratosphere

Q4 2018 data was not very friendly to specialty generic oral solids in Ohio. Unlike other generic oral solids, specialty generic oral solids (at least the top three we found a few weeks ago) sport prices in Ohio Medicaid managed care that remain hopelessly disconnected from NADAC. With these drugs, it appears that pharmacies are getting the margin, and not the PBM … that is until you dig through managed care preferred drug lists (PDLs) and realize that for specialty drugs, patients are apparently being steered to pharmacies owned either by the PBM or the managed care plan. If you missed our work on this, read all about it here.

Flip through the chart gallery below to see what happened to prices of the top three Ohio specialty generic oral solids in Q4 2018.

HIV/AIDS Generics Now Look Like “Spread Drugs”

The fact that we found three HIV/AIDS generic drugs on the Q3 2018 high markup list was a bit of a head scratcher in last month’s Ohio report. First, they are not classified as specialty drugs on any Ohio managed care PDLs. Second, we had heard anecdotes of pharmacies getting paid poorly for these drugs in 2018, They looked and smelled a whole lot like “spread drugs” yet were experiencing high markups according to the State Utilization Data. We provided a handful of connections CVS/Caremark has to this important class of drugs, but also noted they could all be circumstantial.

Well, the best remedy for questionable data is more data. In Q4 2018, the prices of these three HIV/AIDS generic drugs cratered, putting them firmly in the “spread drug” category, meaning that it appears that PBMs are likely capturing the majority of markups on generic Reyataz (Atazanavir Sulfate), generic Valcyte (Valganciclovir), and generic Viread (Tenofovir Disoproxil Fumarate).

Flip through the chart gallery below and take a look. In Q4 2018, Ohio managed care PBMs paid pharmacies below invoice acquisition cost to dispense Atazanavir. Interestingly, the markups on Tenofovir and Valganciclovir remain a bit elevated, but rather than guess why, we’ll just wait for more data this time.

One more quick note before we move outside of Ohio…

If the data was publicly-available, our next step would be to study the market share by pharmacy for this group of drugs in the state. We are curious whether rates being reported by the MCOs for a generic drug are in any way correlated to which pharmacies are dispensing the drug? Of course, that data is not public, so we can’t do this work. But Medicaid departments should have this data available, and should be able to assess whether there is any correlation between PBM price-setting on generics and market share by PBM/MCO-owned retail/mail-order pharmacies. As vertical integration of the supply chain becomes more and more of the norm, payers and regulators should be keeping a laser focus on conflicts of interest, and how those conflicts could be manifesting into overinflated spending and anti-competitive behavior. Maybe there’s nothing there … but here’s the great part about data analytics – it’s free (correction, it costs us $70 a month for Tableau)! It just takes time, so why not find out?

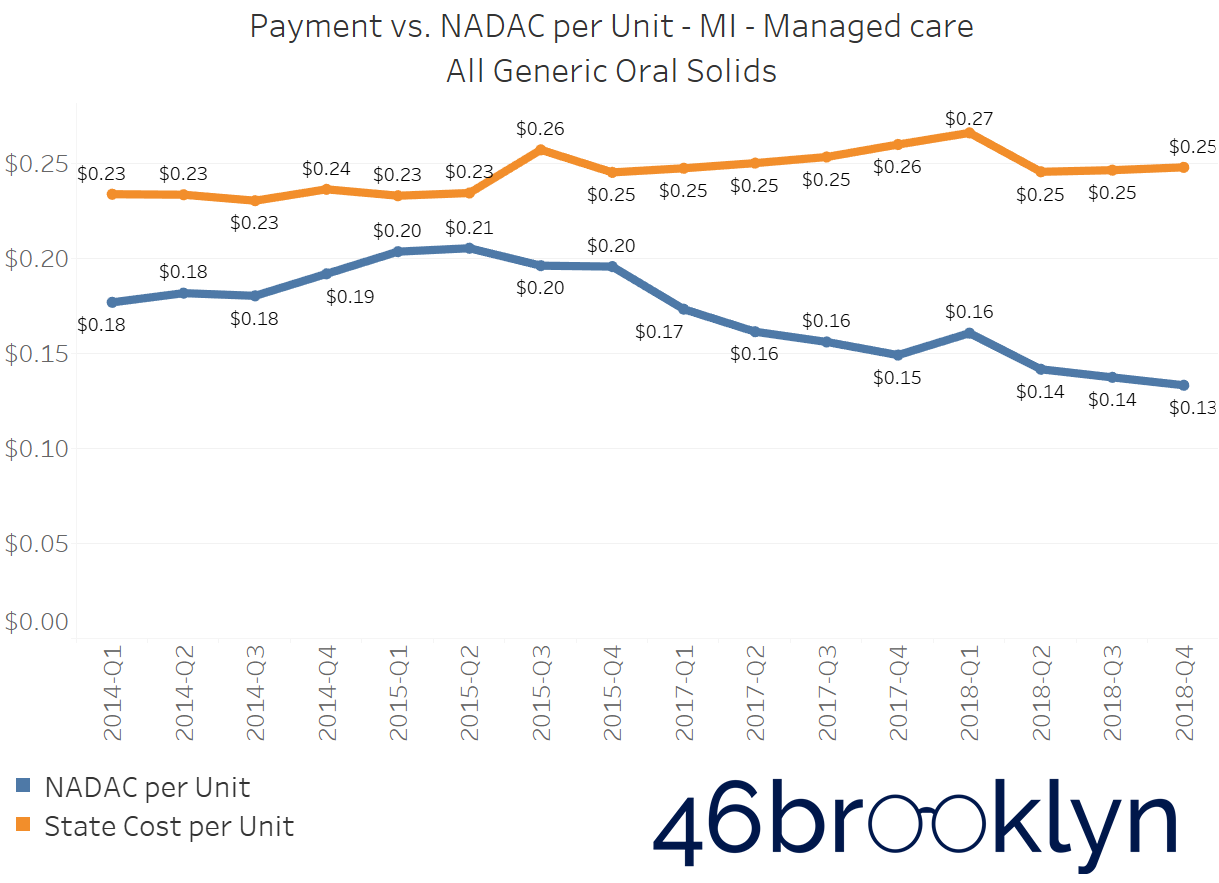

MEDICAID MANAGED CARE MARKUP KEEPS INCREASING ACROSS THE COUNTRY

About a month ago, we observed that in Q3 2018 markup appeared to get worse in many states. Ditto in Q4 2018.

If you select “All” generic drugs within our Heat Map visualization and hover over each state, you’ll find several states where the top line (what the state is reporting generic drugs cost) is stable (or even increasing), while the bottom line (the pre-wholesaler-rebate invoice costs pharmacies pay to acquire the drugs) is decreasing. Of course, when the bottom line falls faster than the top line, drug markup is increasing. The states that once again jumped out to us were Arizona, Massachusetts, Michigan, North Dakota, New Mexico, Nevada, and Texas. We’re adding Maryland, New Hampshire, Pennsylvania and Virginia to that list as well. We’ve embedded figures for all of these states below. As with the chart galleries embedded earlier in this report, click on the arrows to flip from one chart to the next.

New york reported managed care cost data returns!

A few months ago, we noted that New York appeared to have figured out a creative way to solve the drug unit cost problem in managed care: just don’t report cost! While we have no reason to believe this was done on purpose, the timing couldn’t have been any worse for the state to change the way it reported Medicaid managed care utilization data just as light was starting to be shed on markup and spread pricing tactics. A few months later, this appears to have been corrected.

Figure 3 shows what New York’s managed care chart looks like for all generic oral solids. Hopefully, New York will clean up Q2 and Q3 data with next quarter’s release, but at least this is a step in the right direction.

Figure 3

Source: Data.Medicaid.gov, 46brooklyn Research

Look who cracked the Top 20

In our last update on NADAC pricing, we started to move beyond pricing disconnects, and we began to study utilization management (or should we say, mismanagement). One of the drugs that we highlighted was generic Glumetza (most commonly, Metformin ER 1,000 mg Gastric Tablets) which in Q3 2018, sat upon its pedestal carrying a NADAC that was 709 times that of regular old Metformin 1,000 mg tablets. Now, we aren’t clinicians, but we called a few pharmacists and couldn’t find anyone that believed this was a great deal.

However, if Medicaid managed care isn’t spending a significant amount on these drugs, then so what? This is just some random distortion that managed care PBMs have stamped out in their quest to drive lower costs for the states they serve (which is what they will tell you they do).

But sadly, that’s not what happened. In Q4 2018 – which, mind you, is still not even a complete quarter of data – managed care plans collectively spent $3.75 million for 1,705 prescriptions of this generic drug (both 1000 mg and 500 mg strengths, combined), which is a cool $2,200 per prescription.

That number is even more eye-popping when considering that managed care members in Q4 2018 collectively consumed 1,241,555 prescriptions of the original (non-extended release version) Metformin (500 mg and 1,000 mg strengths combined) at a cost of $5.57 million. That’s $4.48 per prescription.

To show you how bad this has gotten, this extremely low-utilization drug amazingly cracked the nationwide Top 20 over $20 this quarter (Figure 4), making it one of the most overpriced drugs in the country.

Figure 4

Source: Data.Medicaid.gov, 46brooklyn Research

It also happens to be two of the largest bubbles within our Q4 2018 Medicaid Markup Universe dashboard (Figure 5).

Figure 5

Source: Data.Medicaid.gov, 46brooklyn Research

Over the past nine months, we have been so focused on pricing disconnects that we may have been missing a much larger problem – poor drug utilization management. To be sure, there are challenges in doing this work because quality drug classification data (to determine therapeutic equivalents) costs money, and money was not something we had readily available when we started our work. But we simply must expand our study of Medicaid to utilization. To that end, we are working on a completely redesigned Medicaid Drug Utilization Dashboard, that will allow the user to view drug utilization in Medicaid relative to Medicaid enrollees (which are available thanks to MacPac). We’ll then work in the coming months to rebuild our tools with a better drug classification backbone, so you can more readily compare utilization across generics within the same class and/or group. Lots to look forward to, for any of you fellow drug pricing nerds.

What are you seeing?

Once again, we set out to write a short and sweet update – and ended up with another long report. But as we wrote earlier, there are just too many potential nuggets of wisdom waiting to be uncovered in this data, and not enough time to dig them all up. So please use the tools we have created for you to keep digging. If you’re seeing any interesting/perplexing movements in the data, please let us know and we’ll investigate further. Thanks for reading!

In the news

Special thanks to the outstanding Kaitlin Schroeder at our hometown newspaper, the Dayton Daily News, for her excellent write-up about our co-founders and our work to restore order to the prescription drug supply chain.

Also, thanks to Jacquie Lee from Bloomberg Law for interviewing our CEO Antonio Ciaccia for his perspective on the one-year anniversary of the release of President Trump’s drug pricing blueprint.

Last but not least, last week, we were honored to have the first major drug supply chain organization formally push back against our research, work, and analysis. That honor goes to the Pharmaceutical Care Management Association (PCMA), the trade group for the PBMs. After seeing the equally flattering and bizarre PCMA-commissioned study from Visante, it finally hit us that our coffee-shop-based drug pricing research of publicly-available CMS data has unbelievably stirred enough up noise for a multi-billion dollar industry to feel compelled to invest in a lengthy retort to our work.

We were honestly torn on how to respond to this. The “ego-driven” part of us wants to methodically tear apart the report, which is not difficult given that most of it takes data limitations that we go to extreme lengths to disclose, and re-labels them as “flaws.” The same part of us also wants to point out that all of the math (see here and here) underlying the entire PCMA #OnYourRxSide campaign comes from the same company that made such cavalier units of measure assumptions in their analysis of our work. If you click on those links above, you’ll also see that both studies were conducted in 2016, before spread pricing really took off.

But ultimately our work (just as the data it relies on) does have its limitations. And you can label them however you want. It doesn’t change the fact that a lot of people were upset when Ohio found $225 million of spread pricing in just one year. That could have been an isolated incident (although our Heat Map dashboard hinted that it was not) until Kentucky reported finding $124 million of spread pricing. And then Georgia went ahead and reported $30 million in spread in just one of the state’s five managed care plans. The work those states did cannot be undone. People are looking for answers on how this could have happened, and our visualizations and writing seem to be addressing this unmet need.

In the end, it’s an honor to have some ceremonial supply chain stones thrown at us, but the beauty of data transparency is that if we take a step back, we can see that this has nothing to do with “us” at all. PCMA’s frustration that hidden industry practices are finally starting to come to light is abundantly clear and the realization that this cannot be undone is understandably unnerving for them and their members. PCMA’s efforts are akin to trying to put toothpaste back into the tube. You can throw a temper tantrum trying to do it, but eventually you have to just calm down and clean up the mess. And if in the end, they truly believe there is no mess to clean up, and that all this pricing controversy is hogwash, then they should look forward to the wave of audits and investigations likely heading their way.

One of the management concepts we absolutely love is called “Six Sigma.” Six Sigma is defined as:

“a set of management techniques intended to improve business processes by greatly reducing the probability that an error or defect will occur.”

Stated more simply, analyze the distortions and mistakes in a process and then learn from them. Then use what you learned to adjust your process. Rinse and repeat, and eventually your process will be defect-free (or close to it).

So taking a page from our friends at Visante, we’ll creatively re-label a term both they and PCMA conveniently like to use: “cherry-picking.” If ultimately this is a big, complicated process, and the goal was to have it run as perfectly as possible, our work is not at all “picking cherries.” It’s finding errors and defects in the system.

Except here is the conundrum. For the taxpayers footing the bill for managed care capitation payments that are based on over-inflated generic drug pricing data, this is a real problem. For the employers that are used as pedestals for the supply chain to stand on, it’s a perpetual struggle. For the senior that is told to cough up hundreds of dollars for coinsurance on a generic drug, only to learn later the drug really only costs a fraction of that, this is clearly a glaring defect. But for the supply chain making money off of such “profit optimization,” this is not a defect at all; it’s a core component of its business model.

But we now have hope that things will change. Clearly no one would read our work if no one thought this was a problem. Instead, more than 15,000 people visited 46brooklyn in April alone. This motivates us to put out more case studies for you to dissect, more visualizations for you to poke around in, better media to help educate the broader public on how this system really works, and new resources to better assist others in doing their own research and seek their own answers.

Thanks again for all of your support throughout what has turned into a very exciting journey.