Same drug, thousands of prices: Crossing Medicare’s Catastrophic Coverage finish line

Opening Ceremony

Back in August 2020, we composed a piece titled, “The Flawed Design of Medicare Part D: A Copaxone Case Study,“ which explored some of the perverse incentives driving coverage decisions within the federal program that is the primary healthcare access mechanism for seniors. At the time, it unlocked a lot of drug pricing learnings that we still find ourselves calling back to, such as the idea of “zombie brands,” the importance of following drug pricing incentives (i.e., the race to catastrophic coverage), and the important with which public policy shapes our drug pricing realities. While much of what we found in that research – which was later referenced in extensive investigations by the Capitol Forum and the U.S. House Committee on Oversight and Reform – still holds a great deal of truth; however, part of what inspired that story is about to end.

As we highlighted back in that Copaxone report, one of the realities of the incentives within Medicare prescription drug coverage was that many health plans received financial rewards if they ‘raced’ into Medicare’s catastrophic coverage phase (e.g., through the use of brand-preferred-over-generic products [zombie brands] or artificially inflated generic drug prices). This was because health plan liability would be low in catastrophic coverage due to Medicare reinsurance being responsible for 80% of drug costs. Over the years, Medicare plans seemed to have been pretty successful in following the reinsurance incentive, as the amount of reimbursement incurred for premiums and direct subsidy were relatively flat (or went down), while the reinsurance amount grew (as seen in the 2024 Medicare Trustee Report; Figure 1). As can be seen in Figure 1, since 2014 premiums have risen approximately 50%, the direct subsidy declined by 85% and reinsurance grew 2.3-fold.

Translation: Inflated drug prices and misaligned health insurer incentives pushed increasing financial burdens onto taxpayers.

Figure 1

Source: 2024 Medicare Trustee Report

To be clear, we weren’t putting out truly new learnings back in 2020. The messed up incentives were already understood by researchers and policymakers well enough that there were proposals at the time that sought to change some of the flawed incentives within Medicare. To be more specific, the House (HR-3) and the Senate (S-2543) both proposed legislation that, back in 2020, would have eliminated the existing coverage gap and drastically reduced the amount of coverage offered through Medicare reinsurance (i.e., catastrophic coverage). While those specific proposals were not enacted, the version of those proposal outlined by MedPAC at the time (Figure 2) looks a lot like what is going to happen to Medicare coverage in 2025 (Figure 3) following changes enacted as part of the Inflation Reduction Act (IRA).

Figure 2

Source: Medicare Payment Advisory Commission (MedPAC)

As can be seen above, in Figure 3, reinsurance percentage is going from 80% down to 20% (for brand drugs only; the applicable drugs above) and 40% for generics (for generics; non-applicable drugs). Additionally, the patient out-of-pocket (OOP) threshold is decreasing from $8,000 to $2,000. Both of these changes warp the “Race to Catastrophic” coverage in significant ways. Reaching catastrophic coverage now means that Medicare plans – not the government – shoulder most of the financial risk (with no ability to shift cost onto Medicare enrollees as they’ll have met the OOP threshold) for the drug, and the lower OOP threshold makes it more likely to reach catastrophic coverage if drug prices are inflated. This incentive realignment is seen as an opportunity to nudge health plans to favor lower drug prices rather than juicing them higher.

Changes to Medicare plan design are a big deal. According to a report by the HHS Office of the Assistant Secretary for Planning and Evaluation (ASPE), these changes to the Part D basic benefit are projected to save people with Medicare an average of 30% in prescription drug costs in 2025. The Congressional Budget Office (CBO) identified billions of dollars of drug-related savings from the various IRA drug-related provisions (however, some of those figures have since been revised). Others have conversely found that some beneficiary cost sharing may go up in Medicare due to slower progress towards the out-of-pocket (OOP) threshold. Still, others claim the passage of the IRA is going to negatively impact access to medicines and materially discourage drug development as we know it.

While we have previously shared what we feel are some of the positives, trade-offs, collateral damage, and negatives within the massive drug policy overhaul, we still don’t have a complete idea of what the future actually holds. Thus, the fact that so many opinions have already been offered, with such a diverse set of takes and conclusions, warrants a little bit closer scrutiny – specifically, scrutiny of actual Medicare drug pricing data.

Parade of Nations

When we wrote our Copaxone report, we mostly focused on the incentives within plan design – namely how favoring a brand drug over a cheaper generic alternative could put both the plan and patient ahead, and the government behind, when financing drug coverage. However, in focusing on the plan design incentives, we largely overlooked the broad controls that health plans and their pharmacy benefit managers (PBMs) have in shaping drug prices in Medicare. These price-setting controls can also speed up or slow down the race to catastrophic coverage. Think of the Medicare plan’s drug prices as their “athletes” – athletes that can run faster or slower than other competitors. In the competition for prescription drug coverage, the price matters in a variety of ways, especially in Medicare. The price can govern things like patient cost sharing (for coinsurance purposes), but also can influence whether seniors reach the catastrophic coverage finish line sooner than others. And since catastrophic coverage is measured as an out-of-pocket (OOP) threshold, then lower prices will take longer to reach the finish line than higher prices (i.e. they’ll run faster to that OOP threshold). So, for better or worse, the IRA fundamentally alters the race, creating new incentives and cost-shifts that can materially change drug pricing realities for all stakeholders in the Medicare prescription drug transaction.

Before we dig in much further, let us review of few pieces of background information to be sure we’re all familiar with the new IRA “race track” and to properly set the table for this analysis and discussion.

The Drug Pricing Race Track

Prescription drug coverage is far from a monolith. There are many different ways with which a prescription drug benefit can be constructed – including within a singular, massive program like Medicare. And while there are rules of the road from CMS that Part D plan sponsors have to adhere to, those plans have a good deal of latitude in their delivery of value (or lack thereof) for Medicare enrollees. Part of the guardrails that CMS constructs is through the development of the standard benefit design, which includes various phases of coverage that enrollees may experience as part of getting a prescription drug benefit through Medicare. As way of a quick refresher, these phases are historically recognized as:

Deductible: Until a certain dollar threshold is reached (i.e., the deductible), Medicare members are required to pay the full price for prescription drugs they obtain (i.e., the amount negotiated between PBM and pharmacy). For 2025, the standard benefit design sets a $540 deductible.

Initial Coverage: After meeting the deductible, the initial coverage phase represents the portion of drug coverage where the plan and the member share in drug costs. Patient cost-sharing amounts are determined by the plan design (the formulary tier of the drug and the corresponding tier value amount – either a flat copay or a coinsurance percentage). The initial coverage phase ends when the initial coverage limit is reached, which for 2025 will be $2,000.

Coverage Gap: The coverage gap, also known as the donut hole, is a temporary limit on what Medicare drug plans will cover for prescription drugs, which historically shifted more costs onto patients. Longstanding efforts have sought to shorten the coverage gap, and in 2025, the coverage gap will no longer exist as a Medicare coverage phase.

Catastrophic Coverage: For members who spend a high amount of money out-of-pocket, the catastrophic coverage protects them from excessive drug expenditures, as after a certain dollar threshold is reached, Medicare members incur no further drug costs in Medicare for the year. In 2025, catastrophic coverage will be reached when members spend more than $2,000.

However, Medicare members are not guaranteed to experience each of these phases. Plans can offer alternative benefits if they’re equivalent (actuarially) in value to the standard benefit or even offer enhanced benefits beyond standard drug coverage benefits. This of course means that the variability in Medicare prescription drug plans are often more than they seem on their surface – at least if the surface we’re referring to is standard benefit design.

Both standard and enhanced benefit plans vary in terms of coverage, deductibles, cost-sharing amounts, utilization management tools (i.e., prior authorization, quantity limits, and step therapy), and formularies (i.e., covered drugs). Again, Part D does have some guardrails on formulary design, including but not limited to, having six ‘protected’ drug classes (where plans are required to cover all drugs within the class); however, which drugs are preferred or which tier a given drug falls into are just some of the formulary differences that can occur plan-to-plan (other athletes beyond price). These differences mean that from a practical standpoint, how one Medicare beneficiary experiences their drug coverage can look a great deal different from how another person experiences theirs (which is generally not the case with traditional Medicare Parts A & B). Add onto plan design differences – the fact that not every Medicare beneficiary receives the same financial assistance (i.e., retiree drug subsidy or the low income subsidy) – and the variability in the way Medicare enrollees experience cost can quickly can become overwhelming.

Ultimately, the variability in possible Medicare enrollee experiences lead many to debate possible Medicare policy changes from the perspective of the standard benefit design; which, while a helpful shorthand, isn’t necessarily an accurate reflection of the totality of the Medicare experience if for no other reason that the majority of Medicare beneficiaries have not enrolled in a plan that directly mirrors the standard benefit design (per the 2024 Medicare Trustees report; finding the specific percentage of enrollees in standard benefit design proved elusive to us). This means that if we want to have a more nuanced discussion about Medicare redesign changes – such as trying to get a sense for the variability that can exist within Medicare (which we may not immediately notice if we focus just on the standard benefit design) – we will need to recognize that some of the helpful shorthand may not accurately reflect what is or is not going to happen. Nevertheless, we shouldn’t let that stop us from digging deeper into the potential future of Medicare, and to that end we developed a tool to give us a better appreciation of the range of the Medicare drug pricing experience such that we might evaluate the potential policy changes in Medicare. Today, we are releasing that tool.

Lighting the Olympic flame

Check out our previous looks at Medicare’s Quarterly Prescription Drug Plan Formulary, Pharmacy Network, and Pricing Information files:

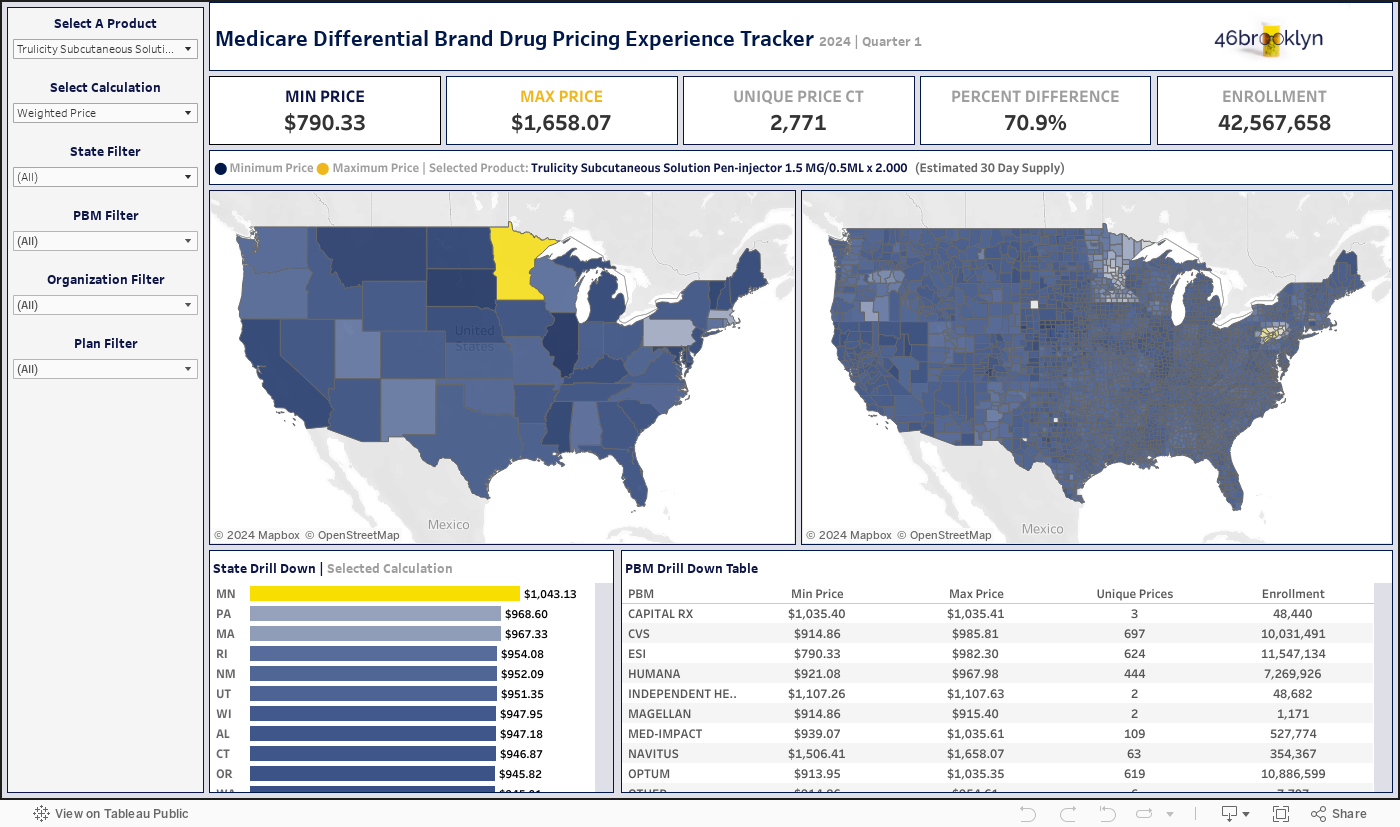

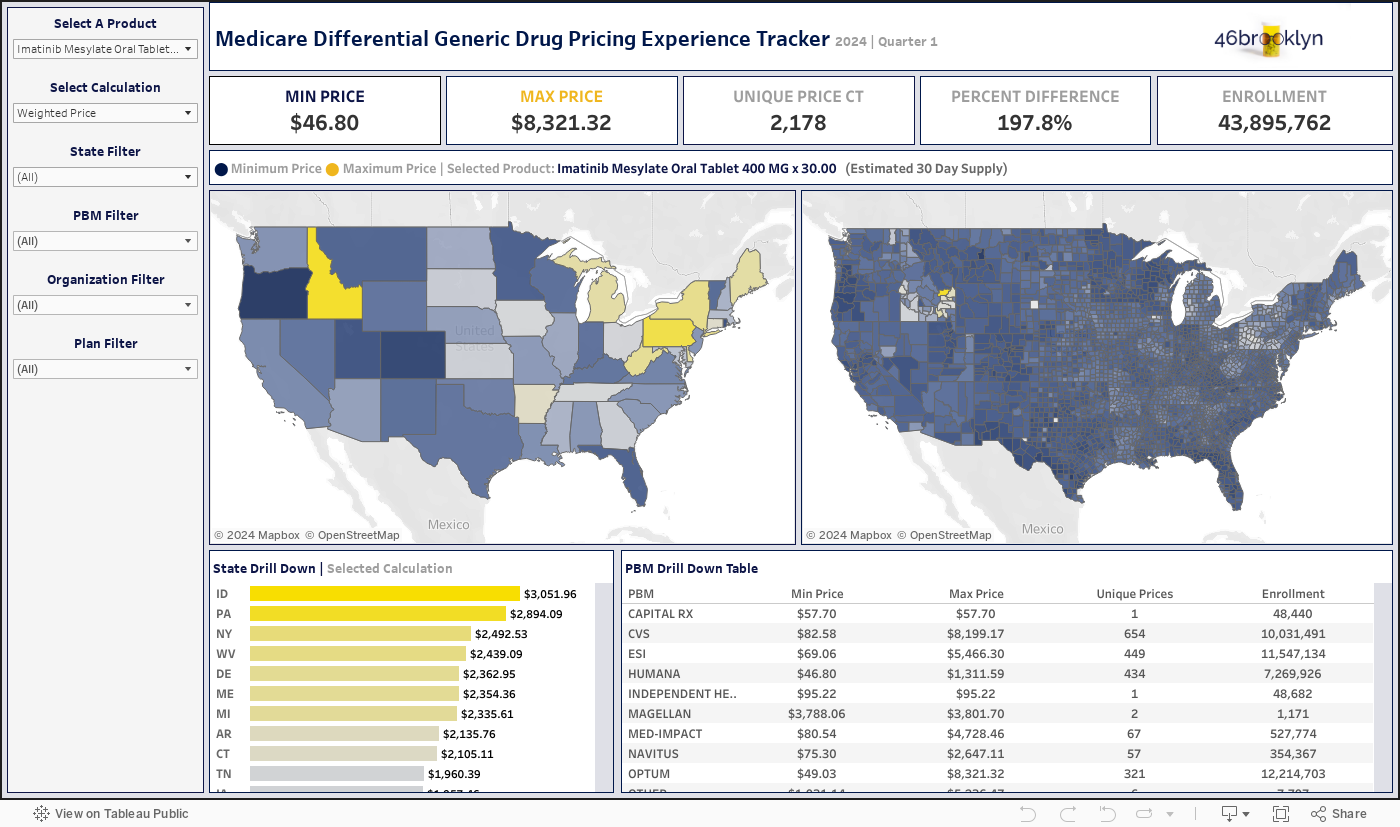

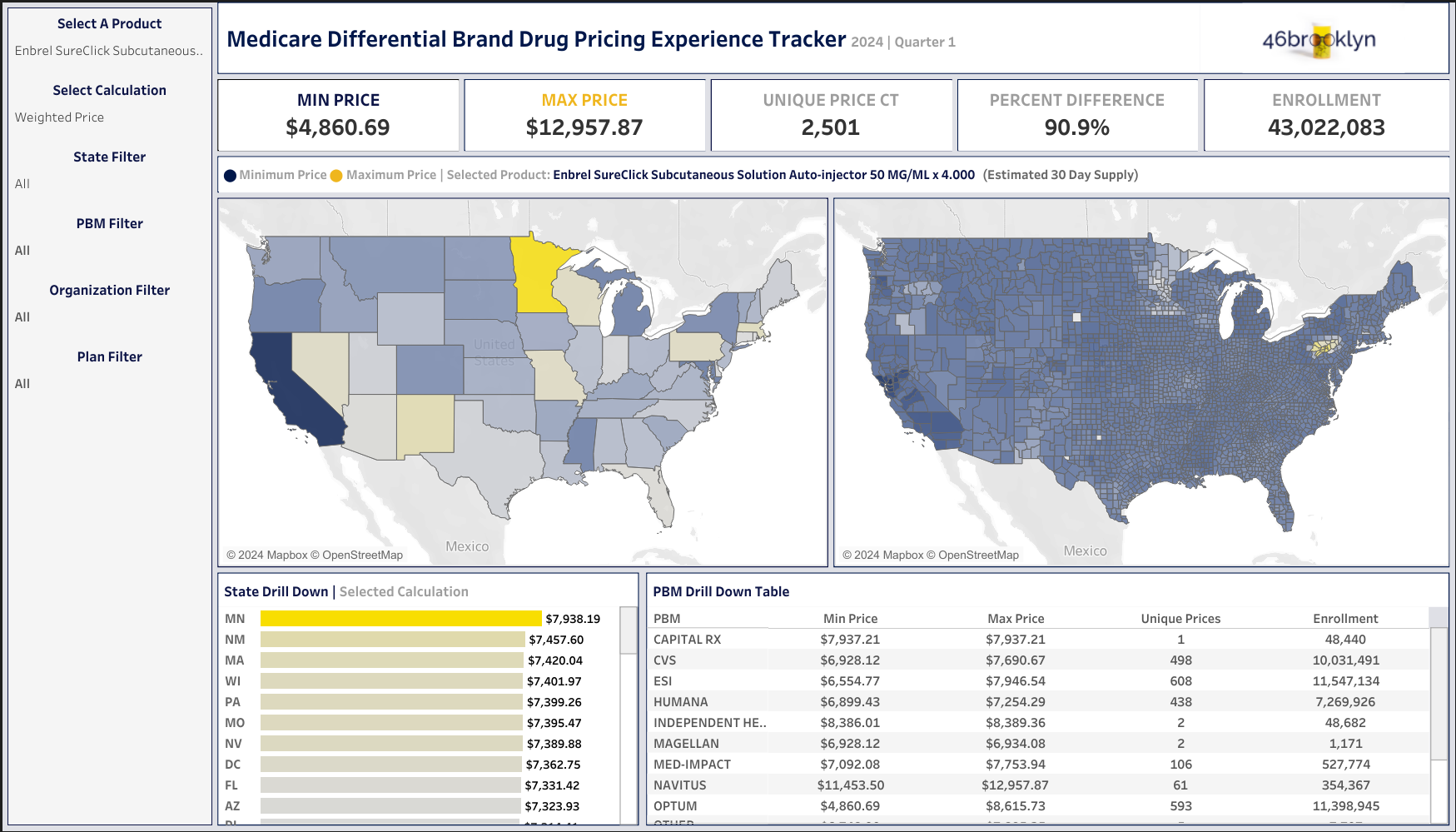

It is no secret that we have become infatuated by the Medicare Quarterly Prescription Drug Plan Formulary, Pharmacy Network, and Pricing Information from CMS. Aside from being a fan of public drug data, we know of no better data source that helps us take an aggregate drug spending trend, such as what exists within CMS’ Part D Dashboard (or the 46brooklyn version), and help to unpack how the aggregate experience may have come to be. Of course, CMS Part D Dashboard data is reported on a deep delay (latest data being reported is 2022 at the time of this report), whereas the quarterly drug plan files are far more current (the file we relied upon covers Q1 2024 – based upon the time we conducted our analysis; even newer files are now available). Nevertheless, having two different sources of data – one informing us of gross drug trends for the entire Medicare program (things like total gross spending, total number of prescriptions, number of members, average gross cost per prescription, etc.) and another letting us see average drug cost per Medicare plan (and any variability therein) – can provide a valuable outline to drug pricing realities within Medicare. And while several of our recent reports have made reference to the data contained therein, we eventually gave into our dashboard desires and built a new one to visualize this impressive data set (using Q1 2024 data, as it took time to put together and the Q2 and Q3 files weren’t out when we started). Note we actually had to build two separate Medicare Differential Drug Pricing Experience Tracker dashboards, because the data was too big to be contained into just one (due to Tableau Public size limitations); so we segregated the data into Brand and Generic dashboards that have the same functionality and logic, but different data inputs.

Data sources and how we created the dashboard

As stated, the vast majority of the data that we used to create this dashboard comes from the Medicare Quarterly Prescription Drug Plan Formulary, Pharmacy Network, and Pricing Information Files available from CMS.gov. Recall that this data provides formulary and pricing for all drugs included on thousands of Part D plans (which includes the Medicare Advantage plans offering prescription drug benefits). Within the data files is a record layout file (i.e., data definition file) that gives us the framework for constructing the dashboard we’re relying upon (Figure 4).

Figure 4

Source: Centers for Medicare & Medicaid Services (CMS)

If you start digging through this mess of data, you will find a couple things. First, CMS says that the pricing information we’re relying upon represents “Plan level average monthly costs for formulary Part D drugs.“ For more details regarding data validations, submissions and quality assurance efforts of CMS you can read up on them here. What we think is important for our readers to understand is that we’re relying upon a field called “Unit_Cost.” This field is defined as the “Average unit cost (e.g. per pill) for specified days supply at in-area retail pharmacies.” We started by extracting this value for each “unique plan” within Medicare (i.e., ContractID, PlanID, SegmentID) and building our database up from there.

The first thing we can do with this file and extracted unit price points is simply observe the minimum and maximum price per Medicare plan and compare that plan’s price against other plans (either within the same Parent Organization or across competing Medicare plan sponsors; this is a fairly straight forward exercise when you unpack the data). However, you’ll also note that the file contains information regarding beneficiary cost sharing, which includes details on cost amounts based upon where the medication is filled by the patient (preferred, non-preferred, and mail-order network pharmacies). We of course had to grab that information for our dashboards as well. From there, we joined in enrollment data from a separate Medicare database (such that we could analyze the plan experience as a function of the plan’s size). Enrollment data was joined based upon the contract and plan information contained above and enabled us to group plan cost by their Parent Organization. We then joined in the PBM the plan was utilizing based upon yet another drug database, PBM payer sheets, and our own industry knowledge (we did not capture every unique PBM, and so we rolled up a few, generally the smaller ones, into an “Other” category).

Next, we added in reference prices so that we would have some basis to compare the stated Medicare average plan price against some benchmark representing some semblance of reality for the drug’s actual cost. Specifically, we used a combination of data sources, which included the Mark Cuban Cost Plus Drug Company (MCCPDC) prescription drug prices (much has been made on potential savings to Medicare with Cuban prices, so it seemed appropriate), as well as an actual pharmacy acquisition cost for medicines estimated based upon National Average Drug Acquisition Cost (because NADAC is not published for all drugs that CMS has purview over – as NADAC is a retail pharmacy drug pricing survey [not a full survey] – we filled in any of the NADAC gaps with the Texas Medicaid stated acquisition cost for pharmacies). In so doing, all of our drugs have a benchmark price we can compare to, and some have a MCCPDC price we can compare to. Finally, we took all of our unit-based pricing information and multiplied the unit by the average number of units per prescription derived from our experience (Dashboard highlights the assumed units and in the rare occasion reports at the unit price if we do not have a basis to make an estimate for typical per Rx dosing). Although not a perfect system, we display the units we’re using on the tracker tools such that you can work backwards to a unit price if you prefer (our experience tells us people prefer to discuss average prescription costs rather than unit costs).

Once we tied together these various data points into one singular data base, the result is our Medicare Differential Brand Drug Pricing Experience Tracker and Medicare Generic Differential Drug Pricing Experience Tracker, which enable the user to select an individual drug (upper left) and evaluate the Medicare pricing information contained within a variety of means (select calculation). Specifically, users can evaluate drug cost as follows:

Weighted Price: Takes each reported unit cost and multiplies it by the plan’s enrollment. Aggregation in a region (i.e., state) reflects the reported prices and enrollment data for that region.

Average Price: Takes each reported unit cost and provides a view of the average price (without weighting by enrollment).

Min Price: Identifies the lowest unit cost reported for the drug in the area (i.e., state or county)

Max Price: Identifies the highest unit cost reported for the drug in the area (i.e., state or county)

Weighted Pref(erred) OOP: Identify the member out-of-pocket (OOP) based upon the drug’s tier and corresponding cost-share amount for that tier for drugs dispensed at preferred network pharmacies under the plan. For drugs that require a coinsurance (i.e., percentage of drug cost-sharing amount), we take the percentage and multiply by the plan’s reported cost. From there, OOP results are weighted based upon plan enrollment.

Weighted NonPref(erred) OOP: Identify the member OOP based upon the drug’s tier and corresponding cost-share amount for that tier for drugs dispensed at non-preferred network pharmacies under the plan. For drugs that require a coinsurance (i.e., percentage of drug cost-sharing amount), we take the percentage and multiply by the plan’s reported cost. From there, OOP results are weighted based upon plan enrollment.

Weighted Mail: Identify the member OOP based upon the drug’s tier and corresponding cost-share amount for that tier for drugs dispensed at mail-order pharmacies pharmacies. For drugs that require a coinsurance (i.e., percentage of drug cost sharing amount), we take the percentage and multiply by the plan’s reported cost. From there, OOP results are weighted based upon plan enrollment.

Difference from MCCPDC: Compare the weighted price against the Mark Cuban Cost Plus Drug Company (MCCPDC) price for the same quantity of drugs. Cost includes the 15% mark-up, dispensing fee, and estimated shipping cost (prices as of June 2024).

Difference from Benchmark: Compare the weighted price against the drug’s corresponding NADAC for the same quantity, except in instances where no NADAC price exists; in which case, the price is compared against the price available within the Texas Medicaid Drug Vendor file (prices as of June 2024).

Note: Not all plans have preferred pharmacy or mail pharmacy network pricing. The weighted price in the tool will reflect weighting based upon plans reporting prices with those characteristics. This means that while the reported weighted price will reflect the price based upon all plans reporting a price for that drug, these OOP prices will not reflect the same number of plans and enrollment (as not all plans will have preferred or mail). In other words, the weighting between the top line weighted price and these OOP amounts will not be the same.

From there, the dashboards display the results of the user’s calculation selection across the nation at an aggregated state and county level. Aggregation is handled in reference to the enrollment-weighted lives for the particular area (either state or county). The dashboard also lets you zoom in to specifics at a state, county, PBM, parent organization, or plan level. While these dashboards will have a dedicated visualization page on 46brooklyn, we embed them here below as well.

Users should note that the information contained within these files can change quarter-over-quarter. Given the scale of data and the effort it took to construct, we do not plan on maintaining this visualization in the long-term on 46brooklyn. But we feel it is important from a disclosure standpoint that what we discuss may change quarter-to-quarter (even if the drug manufacturer does not take a list price change during the timeframe).

Now that we have a new set of dashboards that we can use to contextualize the full range of drug prices that exist within Medicare plans, we can begin to unpack some of the upcoming changes to Medicare in 2025 and beyond.

Let the games begin

To start our analysis of Medicare’s disparate drug pricing journey, we’re going to want a drug (or group of drugs) to focus on, as it helps us explain our observations and poke and prod what Medicare policy changes may look like. Back in 2020, we focused on Copaxone, because it was shocking that a popular brand drug with a generic alternative had maintained so much market share in Medicare despite years of potential generic competition (fast forward the tape, and it appears that issues surrounding Copaxone market share tactics have led to a variety of legal pursuits – Department of Justice, Hagens Berman, Blue Cross Blue Shield of Vermont).

For this analysis, we thought we’d start with some drugs that have been quite popular as of late: the 10 brand drugs selected for price negotiation by Medicare via the Inflation Reduction Act (IRA). And before you think that the recently announced Maximum Fair Price (MFP) for these drugs will make any Medicare drug pricing discussion on them moot, we’d note that those prices are not going into effect until 2026, which means they seem relevant for an understanding of what may happen in 2025 with Medicare plan redesign.

While we know that these 10 drugs accounted for over 20% of gross Medicare drug spend in 2022 (according to the Medicare dashboard), we now know that these drugs will continue to account for 20% of gross drug spending into 2023 (even though that data isn’t in the Medicare Part D dashboard yet). We know this because CMS gave us early insights into 2023 spending when announcing anticipated savings from these drugs with their negotiated prices. As an aside, because CMS said that these 10 drugs represented 20% of gross spending at $56.2 billion, we can also identify that total gross spending for all drugs in Medicare in 2023 should come in at around $280 billion – which means that gross spending in 2023 will grow by approximately $40 billion from 2022, or 17% growth.

We can also estimate the net amount paid for these 10 drugs in 2023 based upon CMS stating that, “the negotiated prices would have saved an estimated $6 billion in net covered prescription drug costs [in 2023], which would have represented 22% lower net spending in aggregate.“ Because CMS provides the gross spending amounts alongside the anticipated dollar difference in net cost, as well as the percentage difference in net spending in the aggregate, we can derive that the current net spending on these drugs in 2023 within Medicare. Based upon a proportionality analysis, current net spending for these drugs must approximate $27.5 billion (such that a $6 billion decrease in net spending would have an anticipated 22% lower net spending amount based upon proportionality). Furthermore, unlike other drugs – where we generally lack information regarding aggregate cost-sharing amounts by patients (the Part D Dashboard does not provide this information) – for these 10 drugs, we understand what the level of cost sharing is because once again, CMS told us that these drugs were associated with $3.9 billion in out-of-pocket spending in 2023 (out of a total $18.9 billion in out-of-pocket spending in 2023; also from the announcement regarding drug price negotiation results).

In selecting Januvia, Novolog (and its rough equivalents), Farxiga, Enbrel, Jardiance, Stelara, Xarelto, Eliquis, Entresto, and Imbruvica for today’s report, we’re selecting some of the drugs with the most information available (i.e., $56.2 billion in gross Medicare spending for these drugs was offset by roughly $28.7 billion in direct and indirect remuneration (DIR) to yield $27.5 billion in net spending with patients paying $3.9 billion in out-of-pocket costs in 2023). We hope that in so doing we’re gaining useful additional context to our evaluation of Medicare drug pricing.

Drug pricing impact on standard benefit design value

To begin our analysis, below we provide a gallery from our new dashboard of the potential 2024 prices for these IRA-targeted medications in Medicare based upon the CMS-published drug pricing data that feeds the tool’s insights (Note: the gallery is composed of the highest strength of the product, as multiple strengths exist and the tool is dose specific).

According to the negotiation data we reviewed earlier, the aggregate net experience for these 10 IRA drugs is an approximate 49% rebate offset to their list prices (i.e., $28.7 billion in assumed Medicare DIR out of $56.2 billion in gross costs). However, despite the low net costs, these brand products have gross price ranges where the maximum price can be two to four times the minimum price (Figure 5).

Figure 5

Source: 46brooklyn Research analysis of CMS’ Medicare Quarterly Formulary & Pricing Files

As can be seen in Figure 5, a drug like Novolog – which took a list price decrease of over 70% at the start of the year – can have a Medicare plan price that is more than double the list price and more than quadruple the lowest plan price (if this sounds like déjà vu, we have already talked about Medicare insulin prices this year). That is a lot of variability in price, as the dollar difference is $166 from minimum to maximum. And while most people would probably say $166 isn’t anything to hand wave away (i.e. our characterization of ‘just’ $166), it seems an appropriate characterization given that a medication like Stelara can have as much as a $32K difference in its lowest observed price in Medicare relative to its highest price. For Stelara specifically, the big three PBMs appear to have thousands of dollars in difference in pricing based upon the various plans they are managing the cost of this drug for (Figure 6):

Figure 6

Source: 46brooklyn Research analysis of CMS’ Medicare Quarterly Formulary & Pricing Files

Although we have already identified that it seems pretty counter-intuitive that a brand medication with a single list price (as measured by WAC) can have many hundreds of different prices in the CMS data, what isn’t really appreciated yet is that when the underlying drug cost is tens of thousands of dollars, a little bit of variability (such as just two-fold) can be a lot of actual dollars difference. As can be seen in Figure 6, while the PBMs Express Scripts (ESI) and Caremark (CVS) have roughly $3K in variance from their minimum and maximum prices for Stelara (certainly not a small number of dollars, but a low percentage delta), Optum has a very large range, which clearly warrants a deeper dive.

When we expand the Optum bucket in the lower right of the dashboard to display the various plan parent organizations OptumRx is contracting with, it appears Kaiser is the primary driver of this range. If we look at the parent organization “UnitedHealth Group plans” (which are part of the same parent company as OptumRx), those plans have a smaller range from minimum to maximum than what OptumRx overall shows (see Figure 7 below).

Figure 7

Source: 46brooklyn Research Analysis of CMS’ Medicare Quarterly Formulary & Pricing Files

Based upon the list price (WAC) for Stelara, the Kaiser minimum price is roughly 60% cheaper. While we cannot know for certain, we have previously highlighted Kaiser’s prices in Medicare in prior reports and have previously assumed that Kaiser’s prices reflect efforts to secure the value of rebates or other discounts up front for its members.

The above also presents us with an opportunity to test our Medicare pricing tracker tools. Based on filtering the data to the Kaiser parent organization “Kaiser Foundation Health Plan, Inc.”, we can identify that a plan like Kaiser Permanente Senior Advantage Basic Solano appears to be one of the plans with the lowest Stelara cost (at least within the state of California, where Kaiser is headquartered).

Figure 8

Source: 46brooklyn Research analysis of CMS’ Medicare Quarterly Formulary & Pricing Files

We can also use Q1 Medicare information to confirm that the drug prices for Stelara that we’re displaying appear accurate (Plan Finder doesn’t tell us what the plan’s cost for the drug will be; only the member’s cost). We view this as a good proof point that we’re getting the data analysis right. But we prefer our tool (call us biased), as it provides an easier means to compare drug prices across plans or across the country than anything else we’ve seen out there.

Figure 9

Source: Q1 Medicare

Of course, it is important to appreciate what such variability in Stelara prices means from the context of the standard benefit design. At the $48K maximum Stelara price, Medicare members would reach catastrophic coverage after just one prescription fill (as members get credit for the 70% discount from the brand manufacturer during the coverage gap). Alternatively, the $16K minimum means that those members would also reach catastrophic coverage after one prescription fill. However, one plan will be getting roughly $38K with the next Stelara fill in reinsurance payments for the drug from Medicare (80% of $48K), whereas the other plan will get just $12.8K per month in reinsurance payments.

If we look at the Part D dashboard, which only has spending through 2022, the average Stelara prescription was roughly $25K (approximately equal to its list price). Rolling that price forward based upon the price increases Stelara has taken since 2022, we would assume that the average Stelara prescription in 2024 would cost approximately $28K. At this level, catastrophic coverage would again be assumed to be reached for the member after the initial prescription fill of the medication, and reinsurance payments going forward would be assumed to be $22K per month.

If gross Stelara payments to pharmacies in 2023 were averaging this $28K amount (i.e., WAC), then the data suggests that part of the way this average price is arrived at is that some plans pay less on average for Stelara, reducing Medicare reinsurance payments when they do (i.e., the $16K claims); however, other plans are pumping up Stelara point-of-sale pricing, increasing potential reinsurance payments from Medicare. This of course begs a couple questions:

When reinsurance is based upon percentage, what is the correct reinsurance payment to apply Stelara from Medicare?

What value is being gained or lost due to Medicare pricing variability?

For example, consider that if past trends hold true, Stelara in 2024 would be paying pharmacies at approximately the manufacturer WAC price. We know that since Stelara also has a NADAC price – which gives us a good idea of the pharmacy’s cost to acquire Stelara – we can now draw estimated comparisons between pharmacy acquisition costs and plan/PBM payments to pharmacies for the same drug.

The NADAC for Stelara is 4% cheaper than the manufacturer’s WAC price (consistent with general brand drug WAC trends), meaning that reinsurance payments would be roughly $880 cheaper per Stelara prescription in the catastrophic phase if price was standardized from WAC to NADAC). At four fills per year for patients established on therapy (first two fills are just four weeks apart for Stelara according to its dosing guide, whereas subsequent fills are 12 weeks apart), this would equate to roughly $3,500 per member in reinsurance savings (which for the 23,000 members who used Stelara – based upon 2023 reported figures – could be over $80 million in savings per year).

If you’re not quite following what we mean, we get it. Stelara is such an expensive medication that it doesn’t necessarily matter whether the price is $16K or $48K (as baffling as that range is, considering that the manufacturer only sets one list price for the drug) for the average Medicare enrollee due to the relative degree with which they are insulated from directly experiencing those steep prices. This is because the enrollee will reach catastrophic coverage with the use of Stelara during the first month of use regardless of whether it is the minimum, maximum, or average price of the medication that prevails.

It so happens that this will likely also more or less be true after the drug has the maximum fair price (MFP) in 2026 (at a negotiated price of $4,695 likely that catastrophic coverage will be reached in one to two prescription fills for a patient). And once a member reaches catastrophic coverage, Medicare enrollees become protected from the wild pricing disparities, because they do not incur any additional drug costs after reaching their OOP max ($8,000 in 2024). So the only entities really impacted by this specific pricing disparity, on its surface, are the Medicare plan and the government (as they’re the parties with financial liability in 2024 Medicare plan design; see Figure 3).

While this disparate Stelara pricing can carry ample financial harm to the Medicare program generally, obviously, not every drug carries carries a sticker price as high as Stelara; as most prescriptions are for relatively inexpensive generic drugs. So, to evaluate the value proposition of variable drug prices a little closer, we would benefit from studying a cheaper drug (i.e., one that doesn’t reach catastrophic coverage after just one prescription fill).

Medicare’s gold medal drug

On an individual drug basis, Eliquis is the biggest medication in Medicare (and has been for a couple years now). More gross dollars are spent on Eliquis therapy than any other drug molecule, with $18.3 billion being spent on the therapy in 2023 (roughly 33% of all the expenditures for the first 10 drugs selected for negotiation).

According to our dashboard, some Medicare plans will pay as little as $484 per month for Eliquis 5 mg, whereas other plans will see costs roughly double that amount – $891 per month. Unlike Stelara, Eliquis is comparatively cheap enough that Medicare enrollees in the standard benefit design cannot be assumed to reach catastrophic coverage after the first prescription. In fact, the low end prices of Eliquis will not be expensive enough to cause the member to fully satisfy their deductible in the standard benefit design in 2024 ($484 is less than the $545 deductible). So, as Eliquis costs are rolled forward for members at the ends of the Medicare drug pricing spectrum, members are going to get different levels of value out of their Medicare coverage (from a standard benefit design perspective) over the year (Figure 10).

Figure 10

Source: 46brooklyn Research analysis of CMS’ Medicare Quarterly Formulary & Pricing Files and Standard Benefit Design

Based upon the pricing delta, member expenditures for Eliquis under the maximum Medicare price are nearly double the minimum price. Of course, we know that the minimum and maximum prices that exist within Medicare do not necessarily exist in direct correlation to the standard benefit design (recall that most members are not in the standard benefit design). Does a member care if their plan is charged $1,000 per month for the drug if they’re paying a flat $50 copay for the drug with no deductible under their plan? We’re not sure they do (KFF reports a lower co-pay is more important than premiums to older adults; note, this conflicts with the historic understanding per MedPAC).

Regardless, the above can demonstrate some of the problems with using the standard benefit design short-hand when evaluating Medicare drug prices. Based upon Figure 10, we may say that patient cost sharing could be reduced relatively simply if all prices were standardized to the low end rather than the average or the high end. Consider, as we did for Stelara, that in 2022, the average cost per Eliquis prescription in the 46brooklyn Part D Drug Pricing Dashboard would appear equal to the manufacturer’s list price at WAC (note the list price stated by CMS for Eliquis in 2023 is $521). If we trend that forward to 2024 (such that we can match the pricing data above to an assumed average gross Eliquis cost for all of Medicare), the minimum price above represents an approximate 10% savings relative to the drug’s list price, whereas the maximum price represents an approximate 70% premium to the WAC price. To put this in perspective, Figure 11 provides a visual representation of these assumed differences:

Figure 11

Source: 46brooklyn Research analysis of CMS’ Medicare Quarterly Formulary & Pricing Files , 46brooklyn Part D Drug Pricing Dashboard, and 46brooklyn Brand Drug List Price Change Box Score data for Eliquis

So, Figure 11 is giving us a sense that just looking at drug prices in isolation can fail to capture the full picture of what is actually going on – particularly in a program as complicated as Medicare. If you chose a plan with no additional member premium and no deductible, might you pay higher monthly drug prices (i.e., Max prices)? That certainly is one possible reason for the pricing variability (Min-to-Max) we’re observing, but not the only one. Nevertheless, it would seem to confirm that manufacturers, and manufacturers alone, are not solely responsible for setting drug prices, at least not fully as it relates to Medicare. Further, these prices beg the question of what the actual value of a prescription drug plan is in Medicare. If we know that brand manufacturer list prices are generally inflated – and that PBMS and health insurers are our mechanism to negotiate more affordable prices – what does it say about their effectiveness when their “negotiation” at best yields an 8% discount and at worst yields a 70% markup to the list price of Eliquis? Or maybe effectiveness is not the right word; perhaps it’s better to ask what their incentives are? Certainly, we’re not the only ones who study drug pricing – we imagine PBMs and health plans spend a great many resources studying internal pricing trends as well as making comparisons to competitors – so what is responsible (i.e., what incentive exists) for so many plans having pricing that looks this way in data? Which in turn raises questions regarding what potential value is pricing variability extracting from plans, taxpayers, and patients?

To explore the impact on patients, we briefly return to our introduction of the 10 drugs for Medicare price negotiation. We begin by trying to reproduce what we did in Figure 11 for all 10 drugs. Because of the significant differences in dollar prices (hundreds of dollars per month vs tens of thousands of dollars per month), we present these as percentage-based plan price differences to the drugmaker list prices in Figure 12:

Figure 12

Source: 46brooklyn Research Analysis of CMS’ Medicare Quarterly Formulary & Pricing Files , 46Brooklyn Part D Drug Pricing Dashboard, and 46brooklyn Brand Drug List Price Box Score list price changes by drug

Figure 12 demonstrates that these 10 IRA negotiation drugs have some potential for significant discounts or premiums relative to drugmaker list price in the Medicare data. When we consider that we know these medications collectively have around a 50% discount off their list price in 2023 after manufacturer price concessions are factored in (and those discounts will likely approach a 60% discount after negotiation takes effect in 2026) – and that the standard benefit design exposes members to 25% of the drug costs in the initial coverage and coverage gap phase – it stands to reason that if plans would lower the price of the drug at the point-of-sale, the member directly benefits to the degree of price savings (especially within the standard benefit design point-of-view). This is because 25% of a smaller number (i.e., the minimum price) is less expenditures than a higher price (i.e., the maximum price). And while this sounds like a “no duh” moment, we bring it up because in talking about the benefits of drug price negotiation, HHS claims that patients will pay around 50% lower in drug costs ($3.9 billion out-of-pocket being reduced by an estimated $1.5 billion). However, is the patient cost share savings from the IRA a result of the negotiation or simply ensuring that drug discounts are getting to the people taking the drugs at the point-of-sale rather than being absorbed by the broader pharmaceutical benefits system?

Said differently, the standard Medicare benefit math suggests that we could have achieved 50% savings by mandating that rebates (which were already 50% off in 2023) be reflected at the point of sale for these drugs. We think this is an important concept, because price disparity in brand drugs (two to four fold difference in price across the program) are potentially problematic beyond just shifting costs onto patients (which is easier to do in the standard benefit if the drug price is higher).

Money from Sick People qualifiers

Readers of 46brooklyn know that our preferred nomenclature for drug rebates is “money from sick people.” We adopted this phrase when we recognized that rebates are generally not directly recognized by those whose drug therapy produces them (i.e. patients). When someone who takes a drug that produces a rebate, the amount of money they pay for their drug is a function of their plan’s benefit design, and most plans are not sharing rebates with patients at the point-of-sale. This is easiest to conceptualize for patients in the deductible phase of their coverage. A patient in the deductible phase pays the full price of their drug while the health plan generates a rebate off the sale of that medicine. We’ve shown the math for a drug like insulin in the past (Money from Sick People Part 1); however, the math works for all drugs that produce a rebate, and the patient pays a price that frequently doesn’t reflect the discount. In Medicare, rebate dollars may be used to “lower premiums” or other things of actuarial equivalent value.

In August 2024, Inmaculada Hernandez et al published in JMCP an estimated rebate value for Eliquis in 2021 of 39.5% of the drug’s list price (Figure 13).

Figure 13

Source: Journal of Managed Care & Specialty Pharmacy, Volume 30, Issue 8

Assuming that Eliquis rebates kept pace with its list price increases (though this may not be accurate), we estimate that rebates for Eliquis in 2024 are approximately $210 per prescription (resulting in a net price of around $300 per prescription). If we remake Figure 10 for Eliquis – this time focusing on the assumed average price in 2024 (i.e., the WAC price) and the hypothetical price if rebates were reflected at the point of sale to benefit member cost-sharing – we would see a roughly 40% reduction in member OOP costs (equivalent to the rebate amount). This is an important observation, as we know that collectively, the net rebates for these 10 IRA drugs prior to negotiation were about a 50% discount. If HHS claims that negotiation lowered Medicare enrollees' cost-sharing by 50%, what exactly about the negotiation — beyond simply accounting for rebates and using a single, consistent price rather than variable prices — produced this reduction in patient costs? In other words, the math seems to suggest that we could have reached the same results (50% cost sharing savings for Medicare enrollees) simply requiring patients get the benefit of their rebates to begin with (i.e., rebates at the point-of-sale; Figure 14).

Figure 14

Source: 46brooklyn Research analysis of CMS’ Medicare Quarterly Formulary & Pricing Files and Journal of Managed Care & Specialty Pharmacy, Volume 30, Issue 8

Of course, there are other potential benefits to securing the discount up front (rather than on the back end) to Medicare. Money from sick people is collected in the rears, which means there are opportunities to dispute paying rebates after the fact that do not exist when the discount is secured up front. One of the primary reasons why a rebate would not be paid to a plan sponsor is because the medication was dispensed by a 340B Covered Entity, and most, if not all, contracts between plans and PBMs state that rebates will not be paid for 340B claims (presumably for the same reason that Medicaid does not collect a rebate on a 340B claim – to prevent duplicate manufacturer discounts).

Think of it this way; if you gave 50% of the list price as a rebate to the health plan (the aggregate rebates we see for these IRA drugs) and a purchase discount to the 340B entity of 50% of the list price (obligation is to give the ‘best’ price discount to 340B covered entities), then you, as the drug manufacturer, would be left with 0% of the list price for your efforts to manufacture and distribute the drug.

We know that the 340B program has grown significantly over time, and approximates ~20% of brand drug claims. This means that roughly two out of 10 claims will not produce the rebate that is expected, which raises the anticipated net cost for the end payer that relies upon rebates (rather than securing a lower up-front discount). However, if the discount is secured up front, at the time the medication is sold by the pharmacy, then this value isn’t actually lost by the payer. From a simple proportionality standpoint, securing the discount up front can be worth up to a 20%+ improvement in net cost (all else being equal) simply because the 20% of claims that wouldn’t produce a rebate (due to 340B exclusion provisions) now produce the up-front discounted price.

Consider an exercise where we track the gross and net price for the minimum price. We can add to this tracker the rebate we anticipate receiving including an assumption that 20% of the rebates do not materialize because a 340B entity dispenses a portion of the claims during the year. With such a tracker, we can begin to evaluate the potential role rebate and list price incentives play in the Medicare ecosystem (Figure 14)

Figure 14

Source: 46brooklyn Research Medicare Eliquis pricing model with assumed lost rebates from 340B claims

We’ve done exercises like the above before, and we understand that the rebate model generally benefits the plan, as they receive rebates that lower their net cost experience that the patient doesn’t see (Money from Sick People Part 1). However, this is the first scenario where we show what the risk is to the plan with rebates (at least when someone else might get the discount).

Based upon the above, perhaps part of the explanation of variable pricing from plans and PBMs in Medicare is the need to create additional opportunities to produce ‘rebates’ when they don’t actually materialize. To be more explicit, what if the reality is that the high prices are artificial and purposeful, and that if necessary extra DIR can be generated from a true-up (pharmacy DIR is not supposed to be a thing in 2024 based upon CMS policy changes, but we know it used to work this way, so let’s just see where the thought experiment leads us). Let’s presume that the reality is that any high plan drug price (i.e., a price above WAC) is reconciled or trued up to the WAC afterwards via a reconciliation process with the pharmacy (the 70% reduction would need to occur roughly one in four times to produce the missing 20% value). If that is the case, then the value generated on those high-cost claims can potentially pay for the claims that don’t produce the rebates that were expected.

Conversely, perhaps one possible reason that pharmacies routinely receive underwater brand reimbursements is that they help pay for claims that did not produce the anticipated rebate (if a minimum price is 10% below the WAC, then an extra two of those claims for a plan that is charged WAC for the drug can help meet rebate guarantees that may be impacted due to 340B (10% savings via pharmacy underpayment + 10% savings via pharmacy underpayment= 20% value generated). By taking extra money from the pharmacy, via a payment below the acquisition price or clawing back overpayments, the net price for the plan can effectively be maintained even if not all claims produce rebates.

The value of front-loading the discount becomes clearer if we remodel the above, but move the net price to the gross (with no rebate); and the impact of the lost rebates is now non-existent (regardless of whether we’re using the min, max, or assumed average perspective to frame our understanding).

Figure 15

Source: 46brooklyn Research Medicare Eliquis pricing model without assumed lost rebates from 340B claims

If you look at the above Figure 15 and compare it to the previous Eliquis model (Figure 14), you will see that Column F above is 16% lower than Column F previously (can’t perfectly fit 20% into a 12-month billing cycle). Whether the claim is dispensed via 340B (where a covered entity may or may not buy it for lower than the low IRA negotiated price) does not impact Figure 15, as it does not rely upon rebates (which may be foreclosed from being collected by 340B status or other rebate exclusions). We bring this up because we know that IRA negotiation secured lower net prices than existed in 2023 for these drugs. The results claimed by HHS is that the negotiation results in 22% net savings. However, that may be underestimated, because we know that the negotiated price applies to 340B covered entities (because it applies to all plans, claims, and benefits within Medicare – it is a universal price). This means claims that historically didn’t produce a discount for Medicare will now produce a discount going forward (which doesn’t seem to have directly been factored into HHS’ analysis but may be responsible for some of the savings that actually result).

Putting it differently: Imagine you run a steel mill, and the mine supplying your iron ore offers a new deal: instead of selling you ore at a low, up-front price, they’ll charge a higher price now and provide a rebate six months later to bring the net cost back down. For your steel mill, this arrangement would require tying up much more capital in inventory, hoping to get some cash back down the line. No reasonable steel mill would likely agree to this setup over the certainty of a lower, up-front price that supports steady cash flow (and the interest yields from that cash flow). But this is exactly how drug rebates work — those due a rebate (plan sponsors) must pay the higher price now and wait for the rebate to come later — bearing the risk that the rebate might never come at all.

So, how large does a rebate need to be to make it worth accepting that risk? It’s an open question, especially as biosimilars try to compete under a rebate system that historically favors established brands. It may be time to rethink this approach — particularly since the brand drug prices we’re paying may not directly reflect the costs we think they do.

Conversely, another perspective worth considering based upon the above is that it would have theoretically been possible to achieve the same 22% savings in Medicare simply by passing rebates through at the point-of-sale. This is not meant to disparage the value of price negotiation for savings – it’s been reported that a subset of the negotiated prices are even lower than the 340B price (i.e., one of the lowest, best price in the market). Rather, it’s meant to highlight the harms that can come to light from variable drug pricing, particularly when that variable drug pricing is unexpected (because many assume that the manufacturer price, and the manufacturer price alone, drives the reality of pricing experience; when in fact it’s possible for a Medicare plan to pay much more than even the manufacturer’s inflated list price for a brand drug). The observation is such that we find ourselves wondering if it came up at all during negotiation which price the manufacturer was actually negotiating against – the price they set or the subjective price that the opaque drug supply chain assigned to their drug therapy?

Closing ceremonies

We know that this stuff is complicated. We know that there are a lot of conflicting opinions on Medicare out there already, and perhaps our adding more insights is not going to help reduce any of the confusion around what is or is not coming under IRA price negotiations. As an Ohio-based team of drug pricing analysts who don’t get to see all the thought, care, and processes for developing public policy in DC, we understand that there are considerations that we are likely missing in this review of the intersection of policy change, Medicare pricing data, and predictions for the future. But perhaps it is that self doubt that is so validating in this space, if for no other reason that we think many believe that the whole drug pricing world is relatively simple and straightforward (i.e., the manufacturer sets the price and we all pay that price).

Before we put our dashboard together on brand drug prices, we were not sure that there was much public understanding of just how variable drug prices, including brand drugs like the list of 10 drugs for Medicare price negotiation, could actually be within the marketplace, and we’re still not sure how despite there being just a single manufacturer price point (an MSRP if you will), hundreds of prices can be yielded by PBMs and plans with massive deltas between the lowest and highest prices – and even yielding “negotiated” prices that even are higher than what we already know is a significantly inflated manufacturer sticker price.

We believe that the lack of transparency and consistency in the drug channel is more problematic than helpful and probably contributes a great deal to the uncertainty regarding potential policy changes. For example, if utilization of these products increases by 30% or more in exchange for slightly lower net prices, then maybe brand manufacturers themselves will embrace the tradeoff for the value it could provide in increasing sales of their medication.

More likely, as most things are, there will be split opinions. Those products who are about to face generic competition that got a MFP established may be more welcome to the establishment of an MFP, as it makes their brand product competitive in the market in ways brands are generally not after generic competition. Alternatively, while CMS and patients welcome the savings, Medicare plan sponsors may not appreciate the threat to their profitability the changes represent – as again these 10 drugs impact 20% of spending. When 20% of spending is effectively standardized, the ability to differentiate your plan and make revenues via normal business operations can come under threat. Does this mean that while these drug prices come down in 2026, other unrelated drug prices will go up for patients, as plans use what opportunity they still have to make money where they can (since they lost the ability to make certain types of money on these specific claims – such as via rebates or higher cost sharing with pricing differentials).

Consider that if HHS is correct, and 22% net savings are achieved, then doesn’t that mean Medicare plans profitability potentially goes down, as their profitability is governed by the Medical Loss Ratio (MLR), which is effectively a profit benchmark tied to net expenditures? Similarly, pharmacy providers appear once again positioned to get the short end of the Medicare policy change stick, as if these 10 drugs don’t lower their WAC price in response to the policy’s negotiated amounts, pharmacies will be buying these drugs at around WAC, getting reimbursed 60% below WAC (via the MFP) and managing the float on all that money for weeks. To be clear, 60% of $56.2 billion (the 2023 gross Medicare expenditure figure) is potentially $33.72 billion in financing that these pharmacies will be responsible for managing on their books. This is before considering that these same pharmacies may see one of their most profitable business lines, their 340B contract relationships, reduce in value by that same 60% discount. What we’re saying is buckle up, because it’s about to be a bumpy ride in pharmacy.

The complexity of the issues at hand cannot be overstated. If PBMs lose their rebates on these drugs, they may indeed shift their focus to favor rebated drugs over those negotiated under the Inflation Reduction Act (IRA), risking a system where premium costs rise as the rebate savings once used to stabilize premiums dwindle. CMS has already stepped in to offset potential premium hikes, but without that rebate support, we could see further financial strain across the system. This reduced cash flow may also exacerbate financial challenges for pharmacies, who could struggle to meet their obligations to wholesalers on time, adding another layer of financial vulnerability.

Further compounding this is the lack of transparency and the troubling inconsistency in drug pricing, where a single manufacturer's price can generate hundreds of PBM-negotiated rates with vast price discrepancies. In short, stakeholders across the pharmaceutical ecosystem are bracing for potentially turbulent shifts.

Shouldn’t it give us pause that a relatively simple transaction sale of a medication relative to a manufacturer list price to a patient with the benefit of insurance is anything but simple? Saying it differently, it seems like all of this could be far simpler than we’ve allowed it to become. Right now, the path forward is fraught with uncertainties, and we must grapple with the possibility that these reforms, celebrated as progress, may not produce the intended benefits across the board. Shouldn’t it give us pause that we cannot definitively say these changes will fulfill their promises? As we move forward, clarity on our policy objectives — and alignment among stakeholders on what “success” means — will be crucial in navigating these uncharted waters.